Insurance companies play a crucial role in protecting individuals and businesses from financial losses caused by unforeseen events. However, what happens when an insurance company itself faces a substantial payout due to large claims or catastrophic disasters? This is where reinsurance comes into play. Often referred to as “insurance for insurance companies,” reinsurance allows insurers to transfer a portion of their risk to another entity, ensuring they remain financially stable even in times of crisis. By mitigating financial exposure, reinsurance helps insurers manage risk effectively, maintain solvency, and continue underwriting policies without fear of excessive losses. In this article, we’ll explore what reinsurance is, how it works, its different types, and why it is a critical tool for insurers in risk management.

What is Reinsurance?

Reinsurance is a financial arrangement in which an insurance company, known as the ceding company, transfers a portion of its risks to another insurance entity, called the reinsurer. Essentially, it acts as insurance for insurance companies, allowing them to mitigate potential losses and maintain financial stability. This process helps insurers manage their exposure to large claims, whether from natural disasters, economic downturns, or unexpected surges in claims. In exchange for assuming part of the risk, the reinsurer receives a premium from the ceding company. Reinsurance enables insurance companies to expand their coverage capacity, protect their assets, and ensure that policyholders’ claims can be met even in extreme circumstances. By spreading risk across multiple insurers, reinsurance strengthens the overall resilience of the insurance industry.

Why Do Insurance Companies Need Reinsurance?

Why Do Insurance Companies Need Reinsurance?

Insurance companies operate in an environment filled with uncertainty, where a single large-scale disaster or an unexpected surge in claims can threaten their financial stability. Reinsurance serves as a safety net, allowing insurers to share their risks with another entity, thereby ensuring they can meet their obligations to policyholders without jeopardizing their financial health. By transferring part of their liabilities to a reinsurer, insurance companies can manage risks more effectively, expand their underwriting capacity, and maintain consistent financial performance. Below are the key reasons why insurance companies need reinsurance.

1. Risk Transfer and Protection Against Large Claims

One of the biggest reasons insurance companies need reinsurance is to protect themselves from large claims that could threaten their financial position. Events like hurricanes, earthquakes, or pandemics can lead to an influx of claims, potentially exceeding the company’s ability to pay. By transferring a portion of these risks to a reinsurer, insurers limit their financial exposure and ensure they can continue paying claims without depleting their capital.

2. Increased Underwriting Capacity

Without reinsurance, insurers may hesitate to provide coverage for high-risk policies, such as large commercial properties, aviation, or high-value life insurance. Reinsurance allows them to increase their underwriting capacity, meaning they can take on larger and riskier policies without fear of overwhelming losses. This benefits both the insurer and policyholders, as it enables broader and more extensive coverage.

3. Financial Stability and Solvency Management

Regulatory bodies require insurance companies to maintain a minimum level of solvency to ensure they can meet their claim obligations. Reinsurance helps insurers comply with these requirements by reducing the amount of risk they retain, effectively strengthening their financial position and preventing potential insolvency in times of crisis.

4. Premium and Claim Stability

Insurance companies face fluctuating claim payouts due to seasonal disasters, economic downturns, and unexpected catastrophic events. Reinsurance provides a cushion against these fluctuations, ensuring that premium rates remain stable over time. This helps insurers maintain a predictable revenue stream while keeping policyholders’ premiums reasonable.

5. Catastrophe Protection

Natural disasters and unexpected catastrophic events can cause massive financial losses for insurers. Events such as hurricanes, floods, wildfires, or large-scale accidents can lead to an enormous number of claims being filed at once. Reinsurance acts as a safeguard, allowing insurance companies to absorb these shocks without jeopardizing their ability to operate or meet their financial obligations.

6. Regulatory Compliance

Insurance regulators require companies to maintain a certain level of capital reserves to protect policyholders. Reinsurance helps insurers meet these regulatory requirements by reducing their net liabilities and ensuring that they have enough financial backing to pay claims, even in extreme situations.

7. Business Growth and Market Expansion

Reinsurance enables insurers to expand into new markets and offer new insurance products without taking on excessive financial risk. By sharing the burden of high-risk policies, insurers can confidently provide innovative coverage options, enter new geographic areas, and serve a broader customer base without overextending their resources.

8. Access to Expertise and Risk Management Support

Reinsurers are highly specialized in assessing, pricing, and managing risks. Many insurance companies rely on their reinsurers for guidance, statistical analysis, and actuarial expertise to improve their risk evaluation processes. This collaboration allows insurers to strengthen their underwriting strategies and make informed decisions about which policies to issue.

9. Arbitrage Opportunities

Some insurers engage in reinsurance arbitrage, where they purchase reinsurance coverage at lower premium rates than what they charge their own policyholders. This allows them to maximize profitability while still ensuring risk coverage, making it an attractive financial strategy for many insurers.

10. Liquidity and Capital Efficiency

Reinsurance frees up capital that insurers would otherwise have to hold in reserves for claim payouts. This increased liquidity allows insurance companies to invest in growth, infrastructure, technology, and customer service improvements while maintaining strong financial health.

How Does Reinsurance Help Insurance Companies Manage Risks?

How Does Reinsurance Help Insurance Companies Manage Risks?

Insurance companies operate in a world of uncertainty, where they must be prepared for large-scale claims due to natural disasters, economic downturns, or unforeseen catastrophic events. A single extreme event can lead to significant financial losses, potentially destabilizing an insurer’s operations. Reinsurance acts as a safety net, allowing insurance companies to transfer part of their risk to another entity, ensuring their financial security and ability to meet policyholder obligations. By spreading risk across multiple insurers, reinsurance strengthens the industry’s overall resilience and enables insurers to underwrite more policies with confidence. Below are the key ways reinsurance helps insurance companies manage risks effectively.

1. Reducing Financial Exposure to Large Claims

Reinsurance protects insurance companies from excessive financial loss by covering claims that exceed a certain threshold. When a major disaster occurs, such as a hurricane or wildfire, the reinsurer steps in to absorb a portion of the financial burden, preventing the insurance company from depleting its resources.

2. Stabilizing Losses and Premium Rates

Insurance markets can be volatile due to fluctuations in claim frequency and severity. Reinsurance helps insurers stabilize their financial results by preventing sudden, massive losses from affecting their balance sheets. This stability enables insurers to maintain competitive premium rates for policyholders.

3. Increasing Underwriting Capacity

Reinsurance allows insurance companies to issue policies with higher coverage limits and take on more significant risks than they would on their own. This expanded underwriting capacity helps insurers grow their business and provide coverage for high-value policies, such as commercial properties, large-scale infrastructure projects, or high-risk industries.

4. Enhancing Financial Solvency

Regulatory authorities require insurance companies to maintain minimum solvency margins to ensure they can meet their claim obligations. Reinsurance reduces an insurer’s liability, helping them comply with these financial requirements and remain solvent even during economic downturns or catastrophic events.

5. Protection Against Catastrophic Events

Natural disasters, pandemics, and unexpected large-scale accidents can lead to an overwhelming number of claims. Reinsurance acts as a financial buffer, absorbing the impact of such catastrophic events, ensuring that insurers can continue to operate and fulfill policyholder claims without going bankrupt.

6. Spreading and Diversifying Risk

Instead of bearing all the risks alone, insurers use reinsurance to distribute risk across multiple entities. This diversification ensures that no single insurance company is overexposed to a particular type of risk, reducing their vulnerability to significant financial shocks.

7. Supporting Business Expansion and Market Growth

By reducing the risk burden, reinsurance enables insurance companies to enter new markets and offer new types of policies. It allows insurers to expand their customer base while maintaining financial security, leading to greater industry innovation and competition.

8. Providing Expertise in Risk Assessment

Reinsurers are specialists in analyzing and pricing risks. Insurance companies benefit from their expertise in underwriting, claims management, and loss prevention strategies, helping them make more informed decisions and improve their overall risk management processes.

9. Ensuring Liquidity for Claim Payments

Reinsurance ensures that insurance companies have enough liquidity to pay out claims promptly. By transferring some of their liabilities to a reinsurer, insurers free up capital that can be used for investment, operational expenses, or business expansion without compromising their ability to settle claims.

10. Encouraging Innovation in Insurance Products

With the financial backing of reinsurers, insurance companies can experiment with new policy offerings that may otherwise be considered too risky. This fosters industry innovation, enabling insurers to develop specialized coverage options for emerging risks such as cyber threats, climate change, and advanced healthcare policies.

How Does Reinsurance Work?

Reinsurance is a crucial financial strategy that allows insurance companies to transfer a portion of their risks to another insurer, known as a reinsurer. This arrangement ensures that insurance companies do not bear the full burden of large claims, enabling them to remain financially stable and continue providing coverage to policyholders. The reinsurance process involves agreements between the ceding insurer and the reinsurer, where risks, premiums, and claim responsibilities are shared based on the contract terms. Below are the key steps and mechanisms that explain how reinsurance works.

1. Risk Identification and Assessment

Before entering a reinsurance agreement, the primary insurer evaluates its portfolio to determine the risks it wants to cede to a reinsurer. This includes assessing high-value policies, natural disaster-prone regions, or industry-specific risks that could lead to large claims.

2. Selection of Reinsurance Type

The insurer decides the most suitable type of reinsurance based on the level and nature of risks involved:

-

- Facultative Reinsurance: Covers individual, high-risk policies that require separate negotiations for each contract.

- Treaty Reinsurance: Covers multiple policies under a single agreement, ensuring automatic coverage for risks that fall within the contract’s scope.

3. Agreement and Contract Formation

A reinsurance contract is established, detailing:

-

- The amount of risk the reinsurer will assume

- The percentage of premiums transferred to the reinsurer

- The claims-sharing arrangement between both parties

- Specific exclusions and limitations of coverage

4. Premium Transfer

The primary insurer cedes (transfers) a portion of the premiums collected from policyholders to the reinsurer in exchange for assuming part of the risk. The reinsurer profits by carefully selecting and diversifying risks while ensuring sufficient reserves for claim payments.

5. Claim Handling and Payouts

When an insured event occurs (e.g., a natural disaster or large-scale accident), the ceding insurer processes the claim as usual. If the claim exceeds the insurer’s retained risk threshold, the reinsurer reimburses the insurer based on the terms of the agreement, reducing the financial burden on the ceding company.

6. Risk Distribution and Retrocession

Some reinsurers further distribute the risks they assume by engaging in retrocession, where they transfer portions of their accepted risk to other reinsurers. This practice helps spread risk even further, ensuring that no single company bears an overwhelming financial burden.

7. Financial Solvency and Compliance

Reinsurance enables insurance companies to comply with regulatory capital requirements and solvency laws, ensuring they have adequate reserves to pay out claims. Many regulatory bodies require insurers to maintain a minimum capital reserve, and reinsurance helps meet these obligations.

8. Periodic Review and Renewal

Reinsurance agreements are reviewed periodically to adjust for changes in market conditions, risk levels, and regulatory requirements. Insurers and reinsurers may renegotiate terms or modify coverage based on past claims experience and future projections.

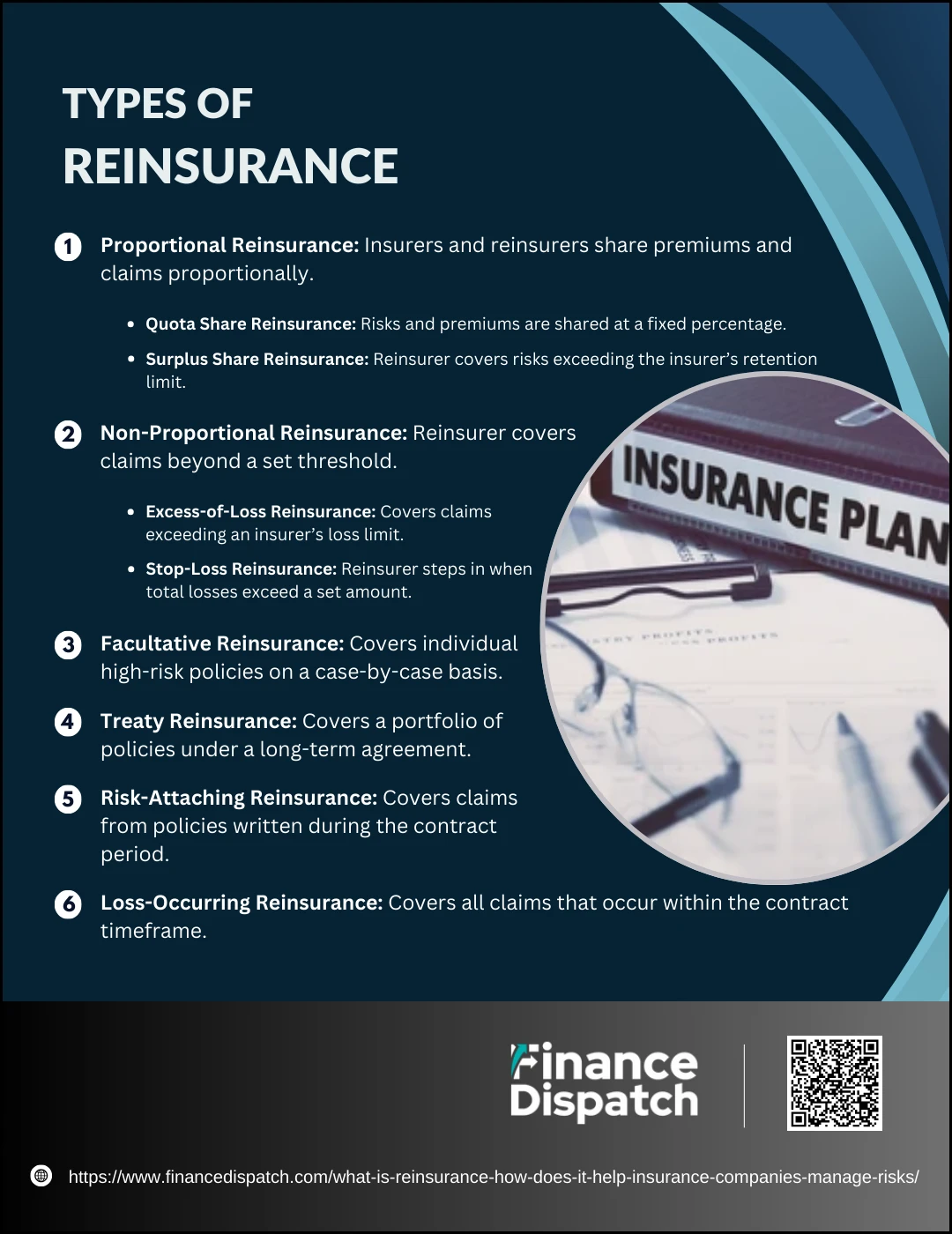

Types of Reinsurance

Types of Reinsurance

Reinsurance is a crucial tool that helps insurance companies manage risk by transferring a portion of their liabilities to another insurer, known as a reinsurer. Depending on the nature of risks involved, insurance companies use different types of reinsurance agreements to balance their financial exposure and ensure stability. The two main categories of reinsurance are proportional and non-proportional reinsurance, with several variations under each. Below is a breakdown of the different types of reinsurance and how they function.

1. Proportional Reinsurance

In this type of reinsurance, both the insurer and reinsurer share premiums and claims in a fixed proportion. The reinsurer receives a percentage of the premiums collected and, in return, covers the same percentage of claims when they arise.

- Quota Share Reinsurance: The insurer and reinsurer agree to share all risks on a predetermined percentage basis (e.g., 60-40). This method helps insurers expand their capacity while maintaining financial balance.

- Surplus Share Reinsurance: The reinsurer covers risks exceeding the insurer’s retention limit. If an insurer sets a threshold for coverage and a policy exceeds that amount, the excess portion is shared with the reinsurer.

2. Non-Proportional Reinsurance

Unlike proportional reinsurance, non-proportional agreements do not require the reinsurer to share premiums equally with the insurer. Instead, the reinsurer only pays claims that exceed a predetermined threshold.

- Excess-of-Loss Reinsurance: The reinsurer covers claims that exceed the insurer’s retained limit, which is particularly useful for catastrophic events. This type helps insurers protect themselves from unexpected financial shocks.

- Stop-Loss Reinsurance: The reinsurer steps in when the insurer’s overall losses surpass a specific limit within a given period, preventing insurers from suffering extreme financial damage.

3. Facultative Reinsurance

This form of reinsurance covers specific, high-risk policies that may not be accepted under broader agreements. It is negotiated on a case-by-case basis, giving both the insurer and reinsurer the flexibility to accept or reject risks individually.

4. Treaty Reinsurance

Unlike facultative reinsurance, treaty reinsurance covers a portfolio of policies automatically. The reinsurer agrees to assume risks for all policies that fall within the scope of the treaty agreement, ensuring long-term coverage for the insurer.

5. Risk-Attaching Reinsurance

Under this type, all claims that arise from policies written during the coverage period are covered, regardless of when the actual loss occurs. This ensures that policies issued within the contract timeframe receive reinsurance protection, even if claims emerge later.

6. Loss-Occurring Reinsurance

This method covers all losses that occur during the contract period, regardless of when the insurance policy was originally issued. It is commonly used for catastrophic events, ensuring financial security for insurers facing sudden, large-scale claims.

Benefits of Reinsurance for Insurance Companies

Benefits of Reinsurance for Insurance Companies

Insurance companies face financial uncertainty due to large claims, catastrophic events, and market fluctuations. Without a risk management strategy, insurers could struggle to pay claims, leading to financial instability. Reinsurance serves as a safety net, allowing insurance companies to transfer part of their risk to another insurer, ensuring their financial security and ability to operate effectively. By leveraging reinsurance, insurers can expand their underwriting capacity, stabilize their financial performance, and protect themselves from unexpected losses. Below are the key benefits of reinsurance for insurance companies.

1. Risk Diversification

Reinsurance allows insurers to spread risk across multiple parties, reducing their exposure to significant financial losses from natural disasters, pandemics, or economic downturns.

2. Increased Underwriting Capacity

With reinsurance, insurers can write more policies and offer higher coverage limits without worrying about excessive risk concentration. This enables them to serve a broader customer base and expand their business.

3. Financial Stability and Solvency Protection

Reinsurance helps insurers maintain financial solvency by preventing large claims from depleting their reserves. This ensures they can meet regulatory capital requirements and continue operations even in challenging times.

4. Protection Against Catastrophic Losses

Events such as earthquakes, hurricanes, and pandemics can generate massive claims. Reinsurance cushions the financial impact, allowing insurers to absorb these losses without jeopardizing their ability to pay future claims.

5. Stabilization of Claims Payouts

Insurance claims can fluctuate unpredictably, causing financial strain. Reinsurance provides a consistent cash flow by balancing high claim periods with financial support from reinsurers.

6. Competitive Pricing and Premium Stability

By mitigating financial risks, reinsurance enables insurers to maintain stable premium rates for policyholders, avoiding drastic increases due to unexpected claim surges.

7. Regulatory Compliance

Many jurisdictions require insurers to maintain a minimum solvency margin to ensure they can fulfill their claim obligations. Reinsurance helps meet these regulatory requirements by reducing net liability.

8. Access to Expertise and Risk Management Insights

Reinsurers have deep expertise in risk assessment and loss prediction. By partnering with them, insurers gain access to advanced risk modeling, claims management strategies, and industry insights to improve their decision-making.

9. Business Expansion and Market Entry

Reinsurance allows insurers to enter new markets, offer specialized products, and cover high-risk industries by sharing the financial burden with reinsurers. This fosters growth and diversification.

10. Liquidity Enhancement and Capital Efficiency

By transferring a portion of their risk, insurers can free up capital that would otherwise be reserved for claim payments, enabling them to invest in new opportunities, improve operations, and enhance customer service.

Reinsurance vs. Coinsurance What’s the Difference?

Both reinsurance and coinsurance are risk-sharing mechanisms in the insurance industry, but they serve different purposes. Reinsurance involves an insurance company transferring a portion of its risks to another insurer (a reinsurer) to reduce financial exposure. This helps insurers manage large claims, remain solvent, and expand underwriting capacity. Coinsurance, on the other hand, is when multiple insurance companies share the risk of a single policy for one insured entity. This ensures that no single insurer bears the entire financial burden of high-value policies. Understanding the differences between these two concepts is crucial for insurers and policyholders alike.

Comparison Table: Reinsurance vs. Coinsurance

| Feature | Reinsurance | Coinsurance |

| Definition | A risk management strategy where an insurer transfers a portion of its liabilities to a reinsurer. | A coverage arrangement where multiple insurers share a single policy’s risk. |

| Purpose | To reduce financial exposure and enhance underwriting capacity. | To distribute the risk of a high-value policy among multiple insurers. |

| Parties Involved | A ceding insurance company and a reinsurer. | Two or more insurance companies covering a single insured entity. |

| Risk Sharing | The reinsurer assumes a portion of the primary insurer’s risk. | Each insurer shares a percentage of the total coverage and claims liability. |

| Premiums | The ceding insurer pays a portion of the policyholder’s premium to the reinsurer. | Each insurer receives a share of the premium based on their coverage portion. |

| Claims Handling | The primary insurer processes claims and gets reimbursed by the reinsurer. | Each insurer directly handles claims in proportion to their share of the policy. |

| Applicability | Used by insurance companies to protect themselves from financial strain. | Used for policies that require large coverage amounts beyond one insurer’s capacity. |

| Example | A home insurance company buys reinsurance to protect against large-scale disaster claims. | A company with a $100 million property policy may have four insurers each covering 25%. |

Challenges and Limitations in Reinsurance

Reinsurance is essential for helping insurers manage risk, maintain financial stability, and expand their underwriting capacity. However, it comes with several challenges that can impact its effectiveness. Economic uncertainties, regulatory complexities, and increasing catastrophe risks pose significant hurdles for both insurers and reinsurers. Below are some key challenges and limitations in reinsurance.

Key Challenges and Limitations in Reinsurance

- High Costs – Reinsurance premiums can be expensive, especially after major disasters.

- Limited Availability – High-risk industries and disaster-prone areas may struggle to find adequate coverage.

- Regulatory Complexities – Compliance with different laws across regions can be difficult.

- Counterparty Risk – If a reinsurer becomes insolvent, the insurer faces financial strain.

- Catastrophic Losses – Unexpected events like hurricanes and pandemics can overwhelm reinsurers.

- Market Cycles – Reinsurance pricing fluctuates, making long-term planning difficult.

- Over-Reliance on Reinsurers – Dependence on reinsurance can reduce insurers’ own risk-taking ability.

- Data Limitations – Climate change and emerging risks make accurate risk assessment challenging.

- Delayed Claims Processing – Complex agreements may slow down claim reimbursements.

- Geopolitical Risks – Economic instability and political changes can affect reinsurance markets.

The Future of Reinsurance

The reinsurance industry is evolving rapidly, driven by technological advancements, climate change, and shifting global economic conditions. As risks become more complex and unpredictable, reinsurers must adapt by leveraging data analytics, artificial intelligence (AI), and predictive modeling to assess and price risks more accurately. Climate change is increasing the frequency and severity of natural disasters, leading to higher claims and prompting the industry to develop innovative solutions such as parametric reinsurance and catastrophe bonds. Additionally, the rise of cyber threats and digital transformation is creating new forms of risk that require specialized coverage. Regulatory frameworks are also changing, with a greater emphasis on solvency requirements and financial transparency. Moving forward, reinsurance companies will need to embrace digitalization, diversify their portfolios, and strengthen partnerships with primary insurers to navigate emerging risks effectively. The future of reinsurance lies in agility, innovation, and resilience, ensuring that insurers remain protected against unforeseen challenges in an increasingly uncertain world.

Conclusion

Reinsurance remains an essential pillar of the insurance industry, providing financial stability, risk mitigation, and enhanced underwriting capacity for insurers worldwide. As the industry faces emerging challenges such as climate change, cyber threats, and evolving regulatory requirements, reinsurance must continue to adapt through technological innovation, data-driven risk assessment, and strategic diversification. The future of reinsurance will depend on its ability to embrace digital transformation, develop innovative risk-sharing models, and strengthen global partnerships. By doing so, reinsurers can ensure long-term resilience, enabling insurance companies to operate confidently and fulfill their commitments to policyholders, even in an increasingly uncertain world.