Buying a home is one of the biggest financial decisions most people will ever make, and for many, it’s not possible without a mortgage. A mortgage is a loan specifically designed for purchasing real estate, allowing homebuyers to spread the cost of a property over several years instead of paying the full amount upfront. But how does a mortgage actually work? From understanding loan terms and interest rates to knowing the different types of mortgages available, navigating the mortgage process can seem overwhelming. This guide breaks down everything you need to know about mortgages—what they are, how they function, and what to consider before taking on this long-term financial commitment.

What Is a Mortgage?

A mortgage is a type of loan used to finance the purchase of a home, land, or other real estate. Unlike personal loans, mortgages are secured loans, meaning the property itself serves as collateral for the loan. This means that if the borrower fails to make payments, the lender has the legal right to seize and sell the property through a process called foreclosure. Mortgages are typically repaid over a long period, commonly 15 to 30 years, through monthly payments that include both principal and interest. Depending on the loan type, these payments may also cover property taxes and homeowners insurance. Because a mortgage is a significant financial commitment, lenders evaluate borrowers based on credit score, income, debt-to-income ratio, and down payment before approving a loan.

How Does a Mortgage Work?

How Does a Mortgage Work?

A mortgage is a loan that helps individuals purchase a home without paying the full price upfront. Instead, a lender provides the necessary funds, and the borrower repays the loan in monthly installments over an agreed-upon period, typically 15 to 30 years. These payments include the principal (the amount borrowed), interest (the cost of borrowing), and often property taxes and homeowners insurance. Since the property itself serves as collateral, the lender can seize and sell it through foreclosure if the borrower fails to make payments. Understanding the mortgage process is crucial for buyers to secure the best loan terms and make informed financial decisions.

Steps in the Mortgage Process

1. Applying for a Mortgage

The process begins with a mortgage application, where borrowers provide their financial details, including income, employment status, credit score, and outstanding debts. Lenders use this information to determine the applicant’s eligibility for a loan.

2. Getting Pre-Approved

Before house hunting, borrowers often seek pre-approval, which means a lender evaluates their financial situation and issues a conditional approval for a specific loan amount. This strengthens the buyer’s position when making an offer and demonstrates financial readiness to sellers.

3. Finding a Home and Making an Offer

Once pre-approved, the borrower searches for a home within their budget. After selecting a property, they submit a purchase offer. If accepted, they move forward with securing the mortgage and completing other necessary steps before finalizing the purchase.

4. Mortgage Processing and Underwriting

The lender reviews the borrower’s financial history, orders a home appraisal to determine the property’s market value, and conducts underwriting to ensure all requirements are met. This step ensures that both the borrower and the property qualify for the loan.

5. Closing on the Mortgage

At the closing meeting, all parties sign legal documents to finalize the home purchase. The borrower provides a down payment, the lender disburses the loan funds, and ownership of the property is transferred from the seller to the buyer.

6. Repaying the Mortgage

After closing, the borrower begins making monthly mortgage payments, which include principal, interest, property taxes, and insurance (PITI). Over time, the borrower builds equity in the home. If they complete all payments as agreed, they will fully own the home at the end of the mortgage term.

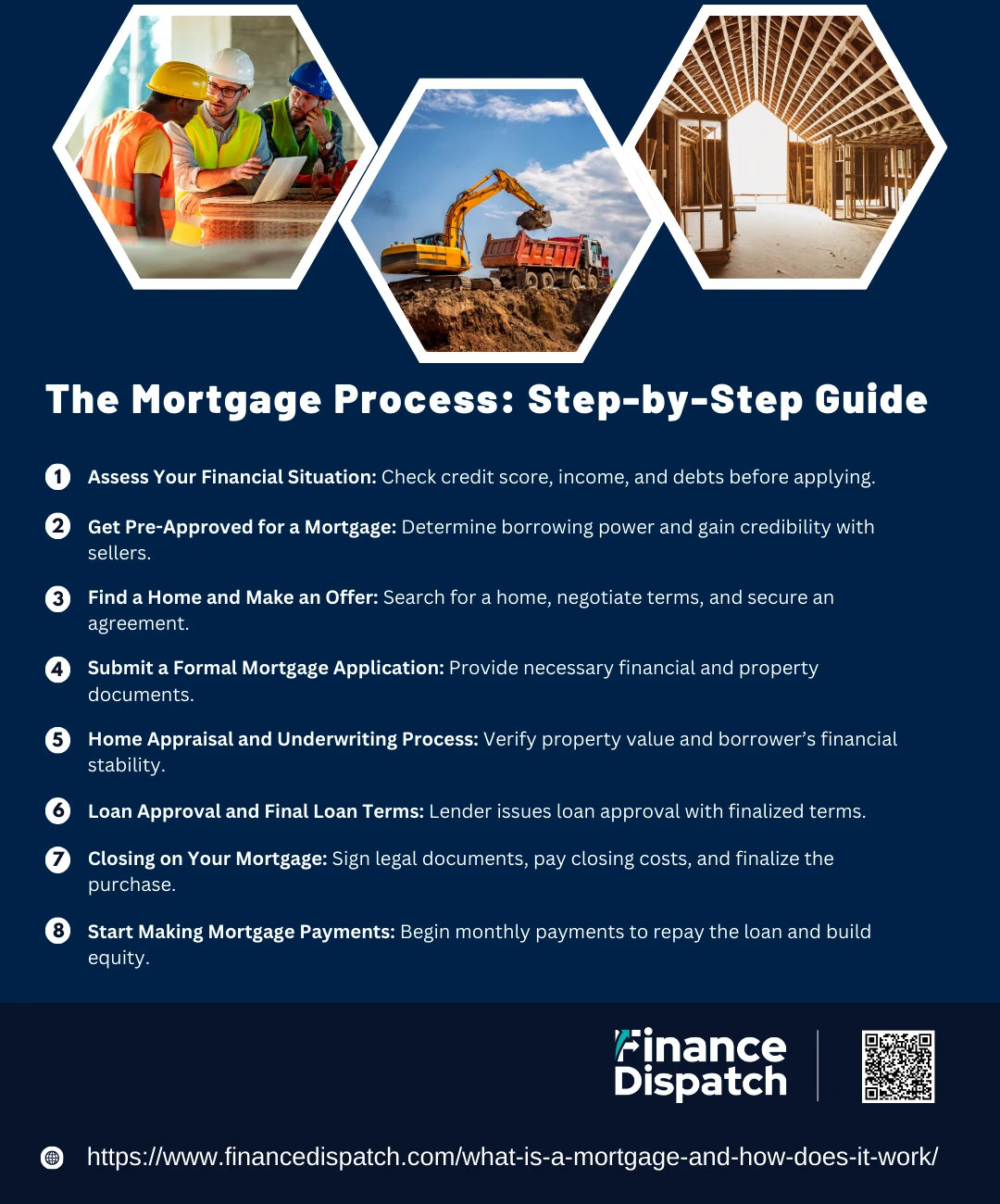

The Mortgage Process: Step-by-Step Guide

The Mortgage Process: Step-by-Step Guide

Buying a home is an exciting milestone, but navigating the mortgage process can feel overwhelming, especially for first-time buyers. A mortgage is a long-term loan that allows you to finance the purchase of a home while repaying it over time through monthly installments. The mortgage process involves several steps, from applying for a loan to closing on your new home. Understanding each step can help you prepare and make informed financial decisions.

Step-by-Step Mortgage Process

1. Assess Your Financial Situation

Before applying for a mortgage, evaluate your financial health by checking your credit score, income stability, and existing debt. Lenders consider these factors when determining your eligibility for a loan.

2. Get Pre-Approved for a Mortgage

A mortgage pre-approval helps you understand how much you can borrow and shows sellers that you are a serious buyer. Lenders review your financial details, including income, debt-to-income ratio, and credit history, before issuing a pre-approval letter.

3. Find a Home and Make an Offer

Once you have a pre-approval, start searching for a home within your budget. When you find the right property, you will submit a purchase offer, which the seller can accept, reject, or negotiate.

4. Submit a Formal Mortgage Application

After your offer is accepted, you need to complete a full mortgage application with your lender. You will provide documentation such as tax returns, pay stubs, bank statements, and details about the property.

5. Home Appraisal and Underwriting Process

The lender will order a home appraisal to determine the property’s value and ensure it aligns with the loan amount. Meanwhile, the underwriting process involves verifying your financial details to assess the risk of lending to you.

6. Loan Approval and Final Loan Terms

If everything checks out, the lender will issue a loan commitment letter, confirming the mortgage approval. This document outlines the final loan terms, including the interest rate, loan amount, and repayment schedule.

7. Closing on Your Mortgage

At the closing, you will sign all required legal documents, pay closing costs (which may include lender fees, property taxes, and insurance), and receive the keys to your new home. Once the lender disburses the loan funds to the seller, the home officially becomes yours.

8. Start Making Mortgage Payments

After closing, your first mortgage payment will be due as per your loan agreement. Monthly payments will typically include principal, interest, property taxes, and homeowners insurance (PITI). Staying consistent with payments helps you build home equity and maintain good financial standing.

Types of Mortgages

Types of Mortgages

Choosing the right mortgage is crucial when buying a home, as different loan types come with unique terms, interest rates, and qualification requirements. Mortgages generally fall into two categories: conventional loans and government-backed loans. Some mortgages offer fixed interest rates, while others have adjustable rates that fluctuate over time. Understanding the different types of mortgages can help you select the best option based on your financial situation and homeownership goals.

Common Types of Mortgages

1. Fixed-Rate Mortgage (FRM)

A fixed-rate mortgage maintains the same interest rate for the entire loan term, ensuring consistent monthly payments. These loans are commonly available in 15-year, 20-year, and 30-year terms, with 30-year fixed mortgages being the most popular.

2. Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage starts with a lower fixed interest rate for a set period (e.g., 5, 7, or 10 years) before adjusting periodically based on market interest rates. ARMs are ideal for buyers who plan to sell or refinance before the rate adjusts.

3. Interest-Only Mortgage

With an interest-only mortgage, borrowers initially pay only the interest for a specified period (e.g., 5-10 years), resulting in lower payments. However, after this period, principal payments begin, often increasing the monthly payment amount significantly.

4. Federal Housing Administration (FHA) Loan

An FHA loan is a government-backed mortgage designed for first-time homebuyers and those with lower credit scores. It allows down payments as low as 3.5%, but borrowers must pay mortgage insurance premiums (MIP).

5. Veterans Affairs (VA) Loan

Available exclusively to military members, veterans, and eligible surviving spouses, VA loans offer zero down payment, no private mortgage insurance (PMI), and competitive interest rates, making them an excellent option for qualified buyers.

6. U.S. Department of Agriculture (USDA) Loan

USDA loans help low- to moderate-income borrowers purchase homes in rural areas with zero down payment. To qualify, the home must be located in a USDA-eligible area, and borrowers must meet income limits.

7. Jumbo Loan

A jumbo loan is a non-conforming loan that exceeds the limits set by Fannie Mae and Freddie Mac. These loans are used to finance high-value properties and typically require higher credit scores, larger down payments, and lower debt-to-income ratios.

8. Reverse Mortgage

Designed for homeowners aged 62 or older, a reverse mortgage allows borrowers to convert home equity into cash without making monthly payments. The loan is repaid when the homeowner sells the property, moves out, or passes away.

How to Qualify for a Mortgage?

How to Qualify for a Mortgage?

Qualifying for a mortgage requires meeting specific financial and credit requirements set by lenders. Before approving a loan, lenders evaluate your ability to repay the mortgage based on your credit score, income, debt, and down payment. Understanding these factors and preparing in advance can improve your chances of securing a favorable mortgage with better terms and lower interest rates. Here are the key factors that determine mortgage eligibility:

Key Factors to Qualify for a Mortgage

- Credit Score Requirements – Most lenders require a minimum credit score of 620 for conventional loans, while FHA loans may accept scores as low as 500-580, depending on the down payment amount. Higher credit scores qualify for lower interest rates.

- Stable Income and Employment History – Lenders prefer borrowers with consistent income and at least two years of steady employment in the same field. Providing recent pay stubs, tax returns, and bank statements helps verify income stability.

- Debt-to-Income Ratio (DTI) – Your DTI ratio compares your monthly debt payments to your gross monthly income. Most lenders prefer a DTI of 43% or lower, but some loan programs allow higher DTIs with compensating factors.

- Down Payment Requirements – Conventional loans often require at least 5-20% down, while FHA loans allow as little as 3.5% down with mortgage insurance. VA and USDA loans offer zero down payment options for eligible borrowers.

- Cash Reserves and Savings – Some lenders require borrowers to have extra savings equivalent to a few months of mortgage payments. Having cash reserves reassures lenders that you can handle unexpected financial challenges.

- Property Type and Loan Program – The type of home you’re buying and the loan program you choose affect mortgage approval. Single-family homes qualify for most loans, but condos, manufactured homes, and investment properties may have stricter requirements.

- Pre-Approval Process – Getting pre-approved by a lender helps determine how much you can borrow and strengthens your offer when buying a home. This involves submitting financial documents for initial lender review.

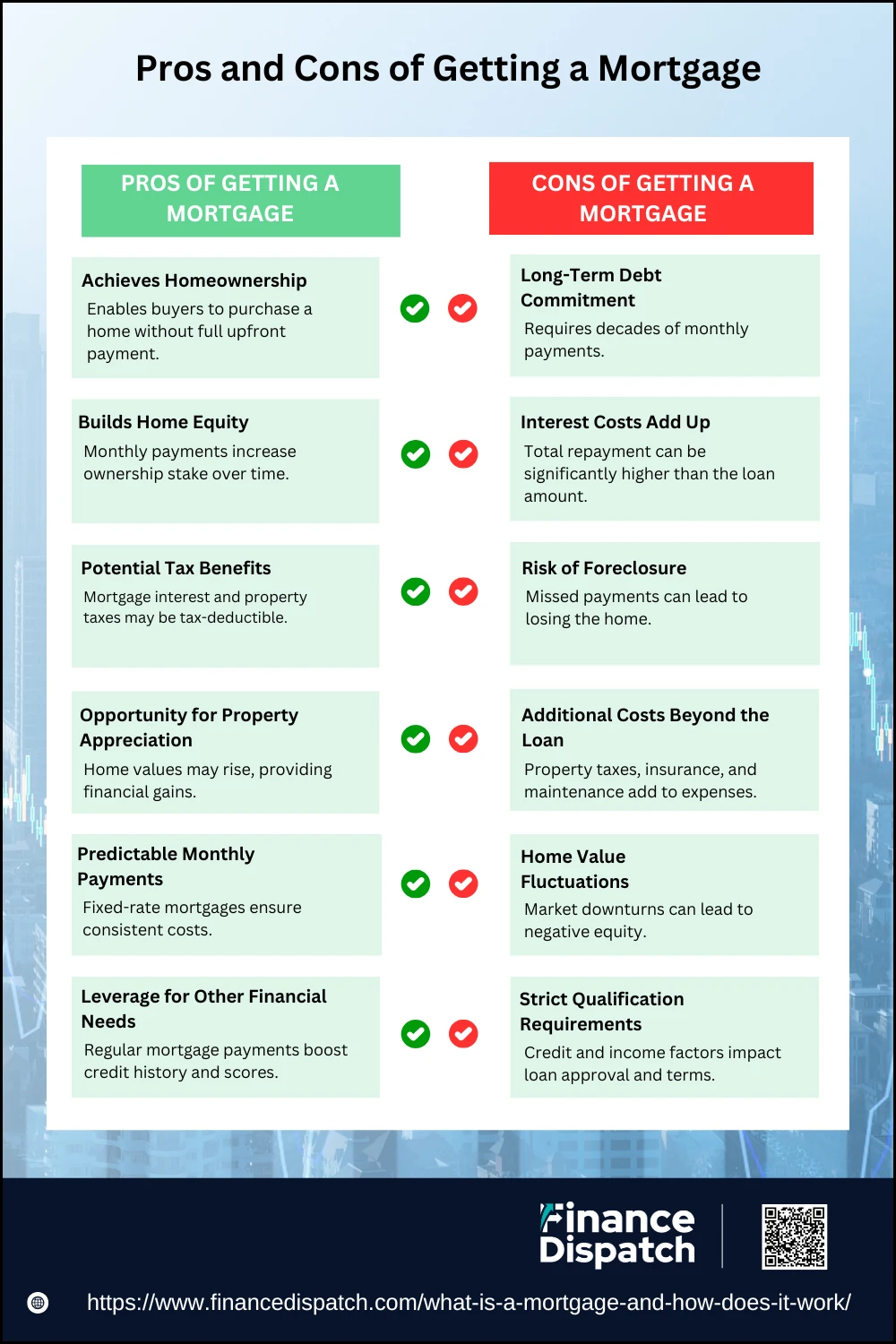

Pros and Cons of Getting a Mortgage

Pros and Cons of Getting a Mortgage

For many people, buying a home is one of the biggest financial decisions they will ever make, and a mortgage is often the only way to afford it. A mortgage allows buyers to spread the cost of a home over many years, making homeownership possible without needing to pay the full price upfront. However, like any financial commitment, a mortgage comes with both advantages and disadvantages. While it provides a pathway to building wealth through home equity, it also involves long-term debt and financial risks. Before committing to a mortgage, it’s essential to understand the pros and cons to determine if it’s the right choice for you.

Pros of Getting a Mortgage

1. Achieves Homeownership

Without a mortgage, many people would not be able to afford a home. A mortgage allows buyers to purchase a property while paying for it gradually, instead of saving for years to buy a home outright.

2. Builds Home Equity

As you make mortgage payments, you gradually increase your ownership stake in your home. This equity can be used in the future for home equity loans, refinancing, or selling for a profit.

3. Potential Tax Benefits

In some cases, homeowners can deduct mortgage interest and property taxes from their taxable income, reducing their overall tax burden. However, tax benefits depend on individual circumstances and tax laws.

4. Opportunity for Property Appreciation

Over time, real estate values often increase, meaning you could sell your home for more than you paid. This appreciation can lead to long-term financial gains and a solid investment return.

5. Predictable Monthly Payments

A fixed-rate mortgage ensures that your principal and interest payments remain the same throughout the loan term, making it easier to plan and budget for housing expenses.

6. Leverage for Other Financial Needs

As your home gains value and you build equity, you can use it to take out a home equity loan or a home equity line of credit (HELOC). These loans can help cover major expenses such as home improvements, college tuition, or debt consolidation.

Cons of Getting a Mortgage

1. Long-Term Debt Commitment

A mortgage is a 15 to 30-year financial obligation, requiring consistent monthly payments for decades. This long-term commitment means you must be financially stable and prepared for ongoing expenses.

2. Interest Costs Add Up

Over the life of the loan, borrowers may pay tens or even hundreds of thousands of dollars in interest, significantly increasing the total cost of homeownership. For example, a 30-year mortgage at 6% interest can result in paying almost twice the original loan amount over time.

3. Risk of Foreclosure

If you miss mortgage payments, the lender has the right to foreclose on your home, meaning you could lose your property and damage your credit score, making it harder to secure future loans.

4. Additional Costs Beyond the Loan

Homeownership comes with extra financial responsibilities, including property taxes, homeowners insurance, maintenance, and repairs. If your down payment is less than 20%, you may also have to pay private mortgage insurance (PMI), increasing your monthly expenses.

5. Home Value Fluctuations

The real estate market can decline, and if your home loses value, you could end up with negative equity—owing more on your mortgage than your home is worth. This can make it difficult to sell or refinance your home without taking a financial loss.

6. Strict Qualification Requirements

To qualify for a mortgage, lenders evaluate credit scores, debt-to-income ratio, employment history, and financial stability. If your credit score is low or you have high debt, you may face higher interest rates, larger down payment requirements, or loan denial.

Mortgage Interest Rates and How They Affect Payments

Mortgage interest rates play a crucial role in determining the cost of homeownership, as they directly influence the amount borrowers pay each month and over the life of the loan. A higher interest rate increases monthly payments and the total amount of interest paid, making the mortgage more expensive in the long run. Conversely, a lower interest rate reduces monthly payments and overall costs, allowing borrowers to save money over time. Interest rates are affected by various factors, including economic conditions, inflation, Federal Reserve policies, and individual borrower qualifications such as credit score and down payment. For example, a borrower with excellent credit and a large down payment may qualify for a lower rate, while someone with poor credit may face higher rates. Even a small difference in interest rates—such as 0.5%—can lead to thousands of dollars in savings or extra costs over a 30-year mortgage. This is why comparing mortgage offers and locking in a favorable interest rate can make a significant financial difference for homebuyers.

Mortgage Myths vs. Reality

When it comes to getting a mortgage, there are many misconceptions that can mislead potential homebuyers. Some people believe they need perfect credit or a huge down payment, while others assume that renting is always cheaper than buying. These myths can discourage buyers from exploring homeownership opportunities or cause them to make uninformed financial decisions. Understanding the real facts about mortgages can help buyers make better choices and avoid unnecessary stress during the homebuying process. Here are some common mortgage myths and the reality behind them.

Common Mortgage Myths and the Truth

- Myth: You Need a 20% Down Payment to Buy a Home

Reality: While a 20% down payment helps avoid private mortgage insurance (PMI), many loan programs allow for much lower down payments. FHA loans require as little as 3.5%, while VA and USDA loans offer 0% down payment options. - Myth: You Must Have a Perfect Credit Score to Get Approved

Reality: While a higher credit score helps secure better interest rates, borrowers with credit scores as low as 500-620 can still qualify for some mortgage programs, depending on the lender and loan type. - Myth: Renting is Always Cheaper Than Buying

Reality: While renting has fewer upfront costs, monthly mortgage payments can be lower than rent in many areas. Additionally, homeownership builds equity over time, providing financial benefits that renting does not. - Myth: You Can’t Get a Mortgage If You Have Student Loans

Reality: Many people with student loan debt successfully qualify for mortgages. Lenders look at debt-to-income ratio (DTI), so managing student loan payments responsibly can still allow you to secure a home loan. - Myth: A Pre-Approval Guarantees Mortgage Approval

Reality: A pre-approval is a strong indicator of how much you can borrow, but final loan approval depends on additional factors like property appraisal, employment verification, and final credit checks. - Myth: Fixed-Rate Mortgages Are Always Better Than Adjustable-Rate Mortgages (ARMs)

Reality: While fixed-rate mortgages offer stability, adjustable-rate mortgages (ARMs) can provide lower initial interest rates, making them a good choice for short-term homeownership or refinancing plans. - Myth: Paying Off a Mortgage Early Results in Penalties

Reality: Most modern mortgage agreements do not have prepayment penalties, allowing borrowers to make extra payments and pay off their loan faster without additional fees. However, it’s important to check loan terms before making large prepayments. - Myth: Mortgage Rates Are the Same at Every Lender

Reality: Different lenders offer varying interest rates, fees, and loan terms. Shopping around and comparing mortgage offers can save you thousands of dollars over the life of your loan.

What Happens If You Can’t Pay Your Mortgage?

What Happens If You Can’t Pay Your Mortgage?

Falling behind on mortgage payments can be a stressful and overwhelming situation, but there are steps homeowners can take to manage the crisis before facing foreclosure. Whether due to job loss, unexpected expenses, or financial hardship, missing payments can put your home at risk. However, lenders often offer options to help struggling borrowers stay on track. If you’re unable to make your mortgage payments, here’s what can happen and the possible solutions available.

Steps to Take If You Can’t Pay Your Mortgage

1. Contact Your Lender Immediately

Ignoring missed payments can make things worse. Reach out to your lender as soon as you realize you’re struggling to pay. Many lenders offer temporary relief options, such as loan modifications, payment plans, or mortgage forbearance.

2. Request a Mortgage Forbearance

A forbearance agreement allows borrowers to temporarily pause or reduce mortgage payments for a set period. This is useful during short-term financial hardships but requires repayment later, either through a lump sum or adjusted monthly payments.

3. Apply for a Loan Modification

If your financial situation has permanently changed, you may qualify for a loan modification, which can lower your interest rate, extend the loan term, or reduce monthly payments to make them more manageable.

4. Refinance Your Mortgage

If you still have a stable income but struggle with high payments, refinancing could help. A refinanced loan replaces your existing mortgage with a new loan at a lower interest rate or longer term, reducing monthly costs.

5. Use Your Home Equity

If you’ve built up equity in your home, consider a home equity loan or line of credit (HELOC) to cover short-term financial difficulties. However, this increases your total debt, so it should be used cautiously.

6. Sell Your Home Before Foreclosure

If you can’t afford your mortgage long-term, selling your home before foreclosure may be the best option. This allows you to pay off your mortgage and avoid credit damage. If your home’s value is lower than your loan balance, a short sale may be an alternative.

7. Consider a Deed in Lieu of Foreclosure

If selling isn’t an option, you may negotiate a deed in lieu of foreclosure, where you voluntarily transfer ownership of your home to the lender to settle the debt. This prevents foreclosure but still impacts your credit.

8. Understand the Foreclosure Process

If payments remain unpaid, the lender can initiate foreclosure, legally taking ownership of your home. The timeline varies by state, but foreclosure can significantly damage your credit score and make it harder to qualify for future loans.

9. Seek Financial Counseling and Assistance Programs

Many government programs and non-profit organizations offer mortgage assistance, financial counseling, or grants to help struggling homeowners. The U.S. Department of Housing and Urban Development (HUD) provides free counseling services to explore options.

Conclusion

Falling behind on mortgage payments can be a stressful experience, but homeowners have multiple options to avoid foreclosure and regain financial stability. Whether through forbearance, loan modification, refinancing, or selling the property, taking proactive steps can help mitigate the impact of missed payments. The key is to communicate with your lender early, explore all available assistance programs, and make informed decisions that align with your financial situation. By understanding your options and acting quickly, you can protect your home, credit score, and long-term financial well-being.