Managing debt is a crucial part of financial well-being, and one way to optimize your loan obligations is through refinancing. Loan refinancing is the process of replacing an existing loan with a new one—often with better terms, a lower interest rate, or a different repayment structure. Whether it’s a mortgage, auto loan, or credit card debt, refinancing can offer significant financial benefits, including lower monthly payments and potential long-term savings. However, it’s not always the right move for every borrower. Understanding when refinancing is a smart decision requires careful evaluation of factors like interest rates, loan terms, and associated costs. In this article, we’ll explore what loan refinancing is, the different types available, and the key scenarios in which it can be a strategic financial decision.

What is Loan Refinancing?

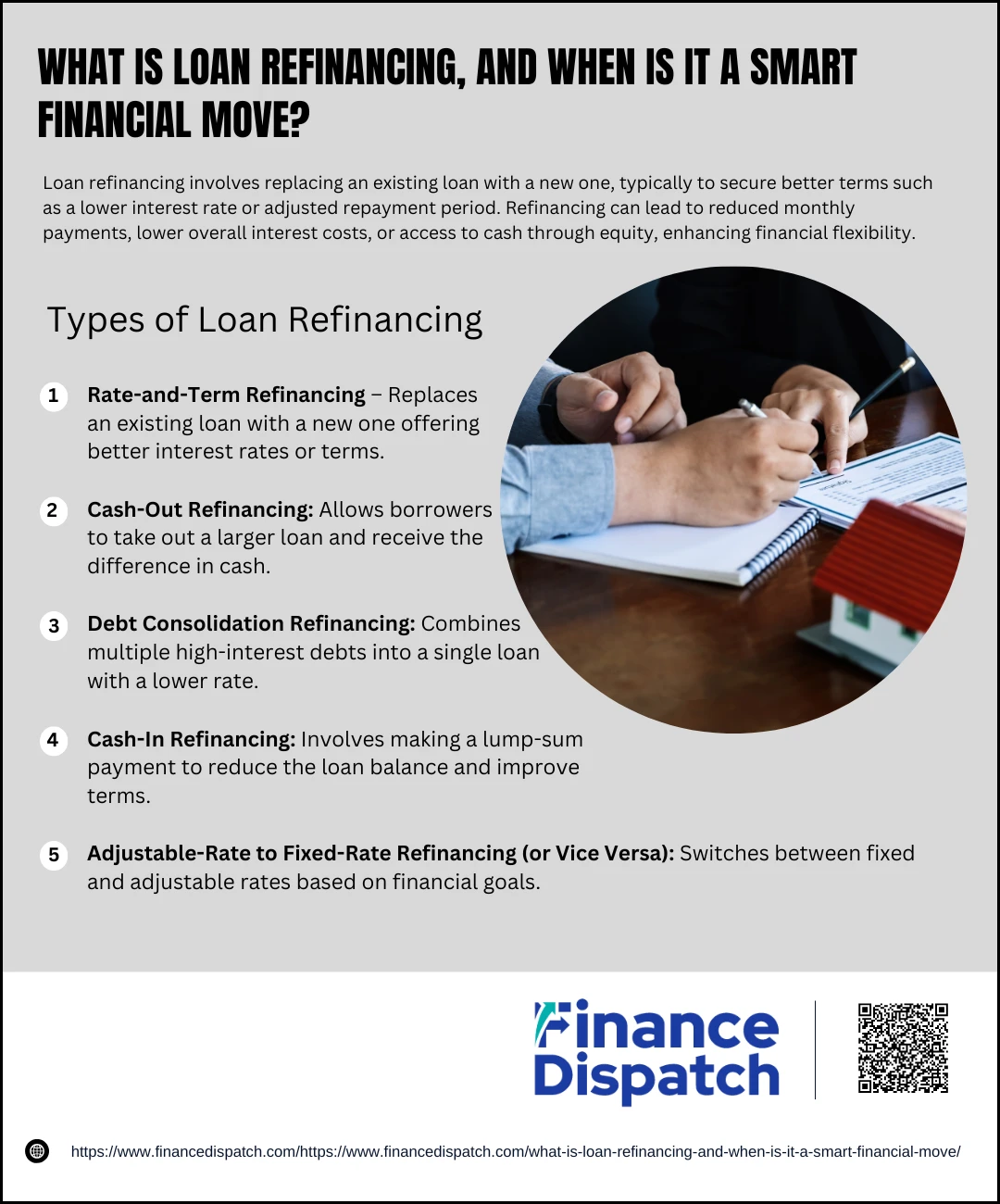

Loan refinancing is the process of replacing an existing loan with a new one, typically with improved terms, such as a lower interest rate, reduced monthly payments, or a different repayment period. This financial strategy allows borrowers to restructure their debt to better suit their current financial situation. Refinancing is commonly applied to mortgages, auto loans, student loans, and personal loans. For example, a homeowner may refinance their mortgage to secure a lower interest rate, potentially saving thousands over the life of the loan. Similarly, individuals with high-interest credit card debt may consolidate multiple balances into a single loan with a lower rate. While refinancing can be an effective way to manage debt and reduce costs, it’s essential to consider factors like closing costs, loan duration, and overall savings before making a decision.

Types of Loan Refinancing

Types of Loan Refinancing

Loan refinancing comes in different forms, each designed to meet specific financial needs. Whether you’re looking to lower your interest rate, adjust your loan term, or access cash from your home equity, choosing the right type of refinancing can help you achieve your goals. Below are the most common types of loan refinancing and how they work.

1. Rate-and-Term Refinancing

This is the most common type of refinancing, where borrowers replace their existing loan with a new one that offers a lower interest rate, better loan terms, or both. The loan amount remains the same, but the improved terms can lead to significant savings over time.

2. Cash-Out Refinancing

With cash-out refinancing, borrowers take out a new loan for a higher amount than what they currently owe and receive the difference in cash. This option is commonly used in mortgage refinancing when homeowners want to tap into their home equity for expenses like home renovations, debt consolidation, or other large purchases.

3. Debt Consolidation Refinancing

This type of refinancing is used to combine multiple high-interest debts into a single loan with a lower interest rate. It is commonly used for consolidating credit card balances, personal loans, or other high-interest debts, making repayment more manageable and potentially saving money on interest.

4. Cash-In Refinancing

In contrast to cash-out refinancing, cash-in refinancing involves making a lump-sum payment to reduce the overall loan balance. This can help borrowers qualify for better loan terms, reduce their monthly payments, or build home equity faster.

5. Adjustable-Rate to Fixed-Rate Refinancing (or Vice Versa)

Borrowers with adjustable-rate mortgages (ARMs) may refinance into a fixed-rate loan to lock in a stable interest rate and predictable monthly payments. Conversely, those with fixed-rate loans might switch to an ARM to take advantage of lower initial interest rates, especially if they plan to sell the property within a few years.

How Does Loan Refinancing Work?

How Does Loan Refinancing Work?

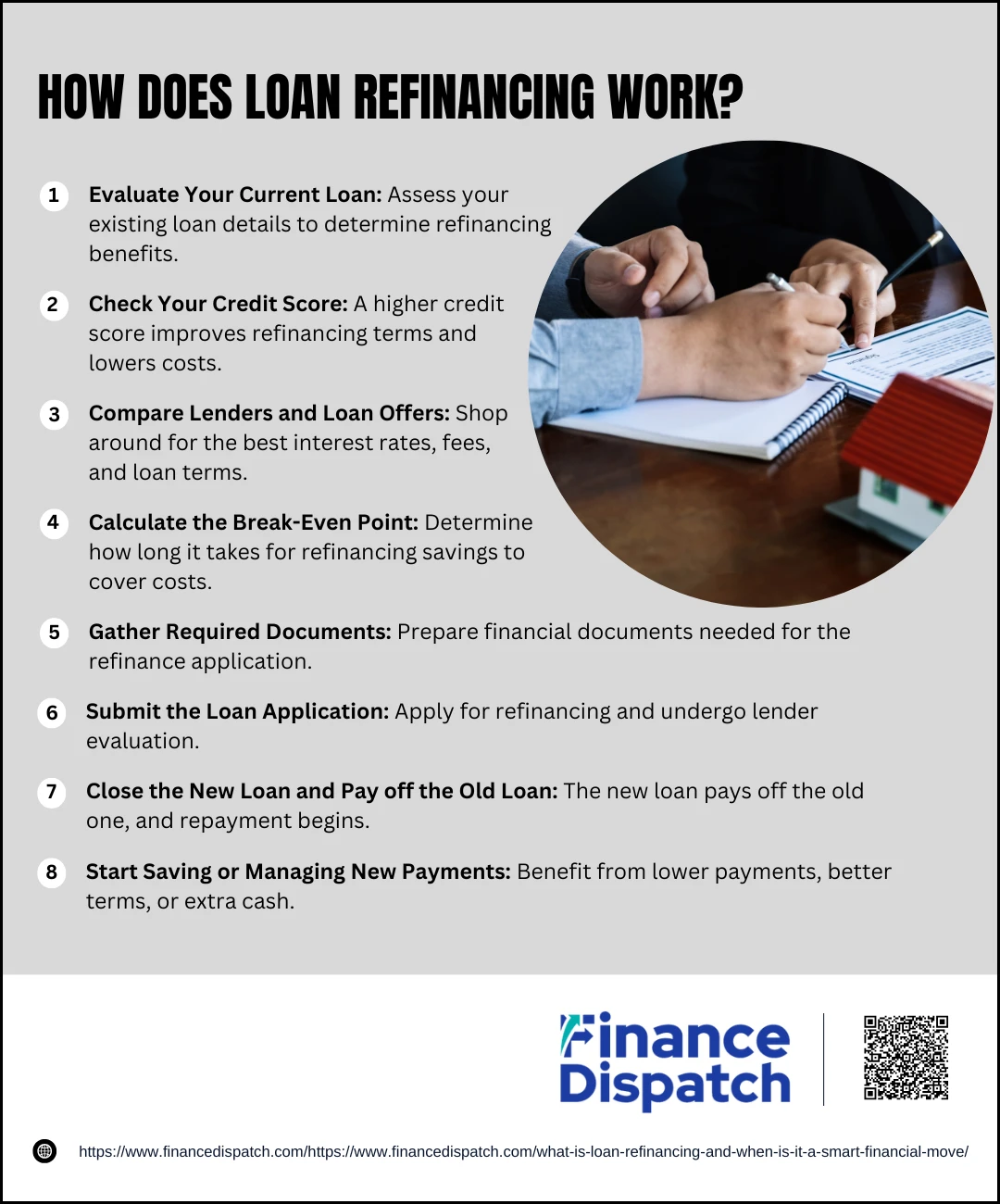

Loan refinancing is a financial strategy that allows borrowers to replace their existing loan with a new one, typically with improved terms such as a lower interest rate, reduced monthly payments, or an extended repayment period. The goal of refinancing is to help borrowers save money, manage debt more effectively, or access funds for other financial needs. The process involves evaluating your current loan, shopping for better offers, applying for a new loan, and closing the old one. While refinancing can offer financial relief, it’s important to consider factors such as closing costs, prepayment penalties, and how long you plan to keep the new loan. Below are the key steps involved in refinancing a loan.

1. Evaluate Your Current Loan

Before considering refinancing, assess the details of your existing loan. Take note of the interest rate, loan balance, monthly payments, and repayment term. Determine whether refinancing will provide financial benefits, such as lowering your payments or helping you pay off debt faster.

2. Check Your Credit Score

Your credit score plays a major role in determining the loan terms you qualify for. A higher credit score can help secure a lower interest rate, while a lower score may result in higher costs or loan denial. Check your credit report for errors and improve your score by paying off debts, making timely payments, and reducing credit utilization before applying.

3. Compare Lenders and Loan Offers

Different lenders offer varying interest rates, fees, and loan terms. It’s important to shop around and compare multiple offers from banks, credit unions, and online lenders. Look beyond interest rates and consider factors like loan fees, repayment flexibility, and customer service.

4. Calculate the Break-Even Point

Refinancing isn’t free—it comes with closing costs and potential fees that can range from 2% to 5% of the loan amount. The break-even point is the time it takes for the savings from refinancing to cover these costs. If you plan to keep the loan beyond the break-even period, refinancing may be beneficial.

5. Gather Required Documents

Lenders require documentation to assess your financial stability before approving your refinance application. Typical documents include pay stubs, tax returns, credit history reports, loan statements, and proof of assets. Having these documents ready can speed up the approval process.

6. Submit the Loan Application

Once you’ve selected a lender, complete the application process. The lender will evaluate your financial history, credit score, and income to determine if you qualify for refinancing. For mortgage refinancing, a home appraisal may be required to assess property value.

7. Close the New Loan and Pay Off the Old Loan

If approved, the lender will issue the new loan and use it to pay off the balance of your existing loan. This officially closes your old loan account. You will then start making payments based on the terms of the new loan.

8. Start Saving or Managing New Payments

After refinancing, you may benefit from lower monthly payments, a shorter loan term, or access to extra cash. However, it’s important to manage your finances wisely. If you consolidated debts through refinancing, avoid accumulating new debt to maintain financial stability.

When Is Refinancing a Smart Financial Move?

When Is Refinancing a Smart Financial Move?

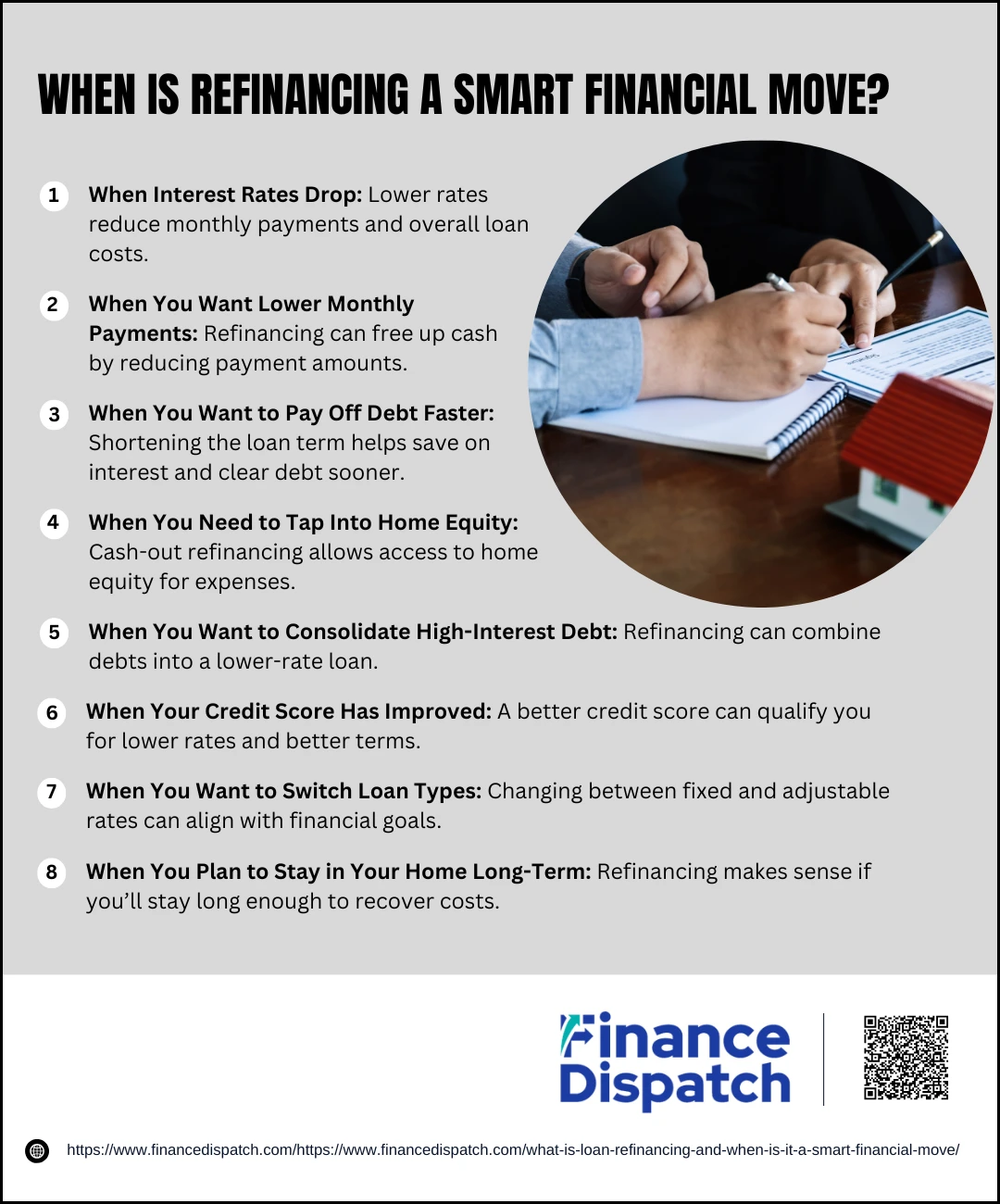

Refinancing can be a great financial strategy, but it’s not always the right choice for every borrower. The key to making refinancing a smart move is ensuring that the benefits outweigh the costs. Whether you’re looking to secure a lower interest rate, reduce monthly payments, or consolidate debt, refinancing can help improve your financial situation if done at the right time. However, factors such as closing costs, loan terms, and your long-term financial goals must be carefully considered. Below are some of the best scenarios where refinancing makes financial sense.

1. When Interest Rates Drop

A lower interest rate can significantly reduce your monthly payments and overall loan costs. Many financial experts recommend refinancing if you can secure a rate at least 1% lower than your current loan. However, even a smaller rate reduction can lead to substantial long-term savings, depending on your loan amount.

2. When You Want Lower Monthly Payments

If your budget is tight, refinancing to a lower interest rate or a longer loan term can help reduce your monthly payments. This can free up cash for other expenses, savings, or investments, making it easier to manage your finances.

3. When You Want to Pay Off Debt Faster

Refinancing can be beneficial if you want to switch from a longer-term loan to a shorter one. For example, moving from a 30-year mortgage to a 15-year term can help you become debt-free sooner and save thousands in interest over time.

4. When You Need to Tap Into Home Equity

A cash-out refinance allows you to borrow more than your current mortgage balance and take the difference in cash. This is often used for home improvements, medical expenses, or other major financial needs. Since mortgage loans typically offer lower interest rates than personal loans or credit cards, cash-out refinancing can be a cost-effective way to access funds.

5. When You Want to Consolidate High-Interest Debt

If you have high-interest debt, such as credit cards or personal loans, refinancing can help consolidate those balances into one loan with a lower interest rate. This can simplify payments, reduce interest costs, and make debt repayment more manageable.

6. When Your Credit Score Has Improved

If your credit score has significantly improved since taking out your original loan, you may qualify for better loan terms. A higher credit score can unlock lower interest rates and more favorable repayment conditions, making refinancing a smart financial move.

7. When You Want to Switch Loan Types

Refinancing is beneficial when switching from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage or vice versa. If you have an ARM and interest rates are rising, refinancing into a fixed-rate mortgage can provide stability. Conversely, if you don’t plan to stay in your home long-term, switching to an ARM could lower your initial payments.

8. When You Plan to Stay in Your Home Long-Term

Since refinancing involves closing costs, it only makes sense if you plan to stay in your home long enough to recover those costs. Calculating the break-even point (how long it takes for savings to outweigh refinancing expenses) is essential before making a decision.

When Should You Avoid Refinancing?

When Should You Avoid Refinancing?

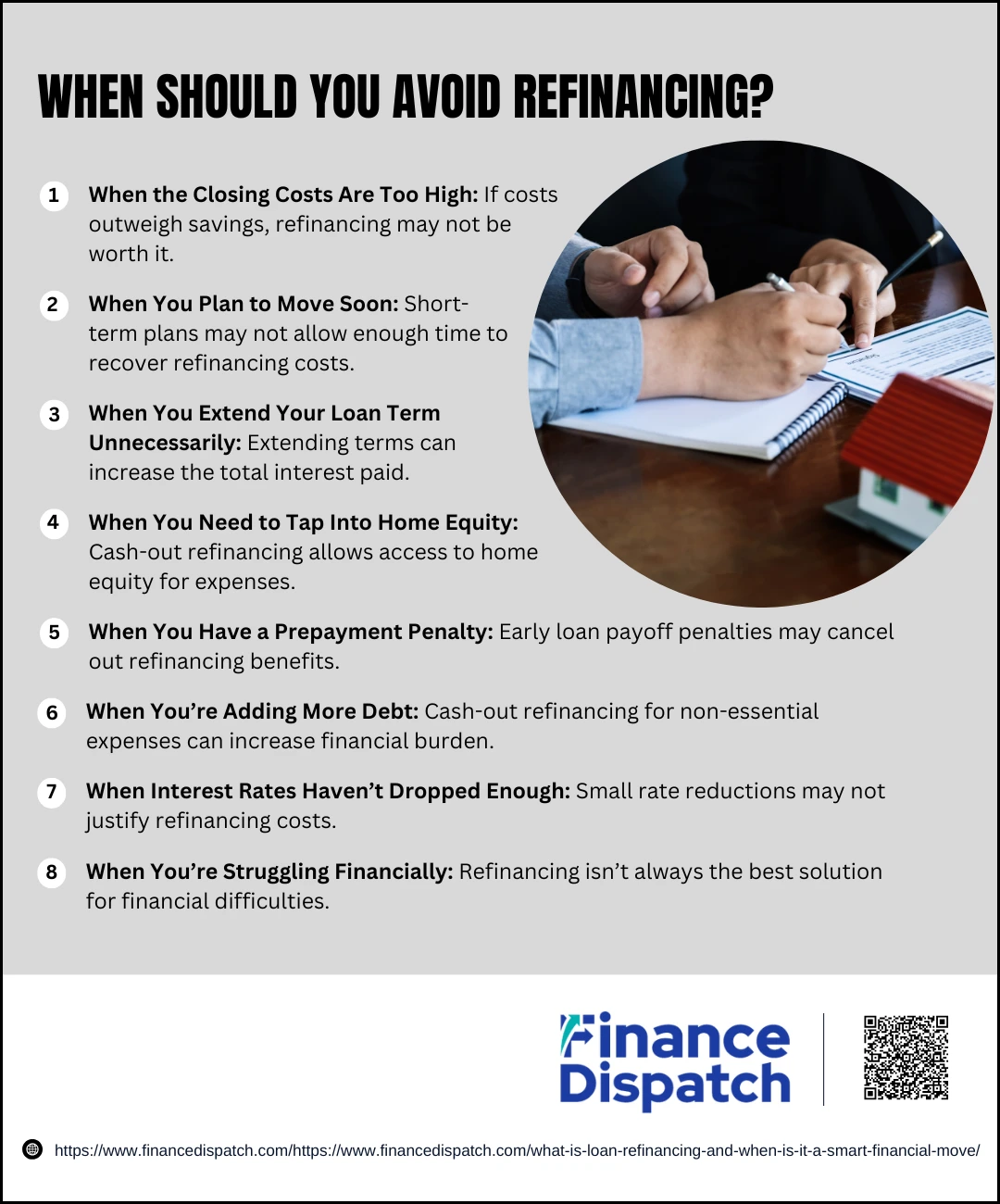

While refinancing can be a great financial tool, it’s not always the right choice. In some situations, the costs, risks, or long-term financial impact of refinancing may outweigh the potential benefits. Factors such as high fees, an extended loan term, or an uncertain financial future can make refinancing a poor decision. Before proceeding, it’s essential to consider whether refinancing truly aligns with your financial goals. Below are some scenarios where refinancing might not be a smart move.

1. When the Closing Costs Are Too High

Refinancing often comes with closing costs that can range from 2% to 5% of the loan amount. If these costs are too high and you won’t save enough to cover them in a reasonable time frame, refinancing may not be worth it.

2. When You Plan to Move Soon

If you’re planning to sell your home or move within a few years, refinancing may not make financial sense. Since it takes time to recover the costs of refinancing, you might not stay long enough to see the savings.

3. When You Extend Your Loan Term Unnecessarily

Refinancing to a longer loan term can reduce monthly payments but may increase the total interest paid over time. If you’ve already made significant progress on your loan, resetting the clock could cost you more in the long run.

4. When Your Credit Score Has Dropped

A lower credit score can result in higher interest rates and less favorable loan terms. If your credit has declined since you took out your original loan, refinancing may not provide the benefits you expect.

5. When You Have a Prepayment Penalty

Some loans have prepayment penalties, which charge a fee if you pay off the loan early. If the penalty is too high, it could cancel out the savings from refinancing. Always check your loan agreement for prepayment terms.

6. When You’re Adding More Debt

If you’re refinancing to take cash out for non-essential spending—such as vacations, luxury purchases, or unnecessary investments—you might be increasing your debt burden instead of improving your financial situation.

7. When Interest Rates Haven’t Dropped Enough

Refinancing usually makes sense when interest rates have significantly decreased. If the rate difference is small, the savings might not be enough to justify the costs associated with refinancing.

8. When You’re Struggling Financially

If you’re struggling to keep up with bills, refinancing might seem like a solution, but it could lead to greater financial issues if not handled carefully. Consider exploring other debt management strategies before refinancing.

Comparing Old vs. New Loan Terms: Is It worth It?

Refinancing can help you secure better loan terms, but it’s important to compare your existing loan with the new loan before making a decision. The key factors to consider include interest rates, monthly payments, total loan cost, and loan duration. While a lower interest rate or reduced monthly payment may seem beneficial, extending the loan term or paying high closing costs could make refinancing less advantageous. To determine if refinancing is worth it, carefully compare the old and new loan terms using the table below.

Old Loan vs. New Loan Comparison

| Factor | Old Loan | New Loan (Refinanced) | Impact |

| Interest Rate | Higher (e.g., 6%) | Lower (e.g., 4%) | Lower rates reduce total interest paid |

| Monthly Payment | Higher (e.g., $1,500) | Lower (e.g., $1,300) | Reduces monthly financial burden |

| Loan Term Remaining | 20 years | 25 years | Longer terms may increase total cost |

| Total Interest Paid | Higher due to higher rates | Lower due to better rates | More savings over time |

| Loan Balance | $200,000 | $200,000 or more (if cash-out) | Balance may increase with cash-out |

| Closing Costs | None (already paid) | 2%–5% of loan amount | Adds upfront costs to refinancing |

| Break-Even Point | N/A | 3–5 years | Time needed to recover refinancing costs |

| Type of Interest Rate | Fixed or Adjustable | Fixed or Adjustable | Switching can affect long-term costs |

| Debt Consolidation | No | Yes (if applicable) | Can simplify payments & reduce costs |

Pros and Cons of Loan Refinancing

Pros and Cons of Loan Refinancing

Refinancing a loan can be a valuable financial strategy that allows borrowers to secure better loan terms, lower interest rates, or access cash for important expenses. Whether refinancing a mortgage, auto loan, or personal loan, the goal is often to reduce overall debt costs, simplify payments, or adjust the loan term to better suit financial goals. However, while refinancing offers many benefits, it also has potential drawbacks, such as high closing costs, extended repayment periods, and possible negative impacts on credit scores. Understanding the advantages and disadvantages can help determine if refinancing is the right choice for your financial situation. Below is a breakdown of the key pros and cons of loan refinancing.

Pros of Loan Refinancing

1. Lower Interest Rates

One of the primary reasons people refinance is to take advantage of lower interest rates. A lower rate can significantly reduce the total cost of the loan over time. For example, refinancing a mortgage from a 6% interest rate to 4% could save thousands of dollars in interest payments over the life of the loan.

2. Reduced Monthly Payments

Refinancing can help lower monthly payments by either reducing the interest rate or extending the loan term. This can provide extra financial flexibility and free up cash for other expenses, savings, or investments. However, extending the loan term may result in paying more interest over time.

3. Shorter Loan Term

For borrowers who can afford slightly higher monthly payments, refinancing to a shorter loan term can help pay off debt faster and save money on interest. For instance, switching from a 30-year mortgage to a 15-year loan can lead to significant long-term savings, even if monthly payments increase.

4. Access to Cash (Cash-Out Refinancing)

Cash-out refinancing allows borrowers to take out a new loan for more than the amount owed on their current loan and receive the difference in cash. This is often used for home renovations, medical expenses, or consolidating high-interest debt. Since mortgage rates are usually lower than personal loan or credit card rates, this can be a cost-effective way to borrow.

5. Debt Consolidation

Refinancing can be used to consolidate multiple debts, such as credit cards, personal loans, and auto loans, into a single loan with a lower interest rate. This simplifies financial management and can reduce the overall cost of debt repayment.

6. Switching Loan Types

Refinancing can allow borrowers to switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage for long-term stability or vice versa to take advantage of lower introductory rates. This flexibility can help borrowers manage payments according to their financial situation and market conditions.

7. Improved Credit Score Benefits

If a borrower’s credit score has improved since taking out the original loan, refinancing can provide access to lower interest rates and better loan terms. This can further reduce borrowing costs and make it easier to manage debt.

Cons of Loan Refinancing

1. High Closing Costs

Refinancing comes with closing costs that typically range from 2% to 5% of the loan amount. These costs include appraisal fees, lender fees, and title insurance. If the savings from refinancing don’t outweigh these costs, refinancing may not be worth it.

2. Extended Loan Term May Cost More

While refinancing can lower monthly payments, extending the loan term means paying more interest over time. For example, refinancing a 20-year loan into a new 30-year loan may reduce monthly payments but could result in paying significantly more in interest over the life of the loan.

3. Prepayment Penalties

Some loans have prepayment penalties, which charge borrowers a fee for paying off the loan early. If a borrower’s existing loan has such penalties, the cost of refinancing may cancel out potential savings.

4. Risk of Increasing Debt

Cash-out refinancing increases the total loan balance. While it provides immediate cash, it also means borrowing more money and possibly paying more in interest over time. If not managed carefully, this can lead to financial strain.

5. Impact on Credit Score

Applying for refinancing results in a hard inquiry on a borrower’s credit report, which can temporarily lower their credit score. Additionally, opening a new loan may impact credit history, which could affect the borrower’s ability to secure other loans in the near future.

6. Break-Even Point Can Take Years

The break-even point is the time it takes for refinancing savings to cover the closing costs. If a borrower plans to move or sell their home before reaching this break-even point, refinancing may not be worthwhile.

7. Uncertain Market Conditions

Refinancing from a fixed-rate loan to an adjustable-rate loan (ARM) can be risky. If interest rates increase in the future, borrowers may end up paying more in the long run. Understanding market trends and future rate expectations is crucial before making this decision.

Steps to Refinance Your Loan

Refinancing a loan can help you secure a lower interest rate, reduce monthly payments, or adjust your loan term to better suit your financial situation. However, the process involves careful planning, research, and financial assessment. Below are the key steps to successfully refinance your loan.

- Evaluate Your Current Loan – Review your existing loan terms, interest rate, and balance to determine if refinancing is beneficial.

- Check Your Credit Score – A higher credit score can help you secure better loan terms, so check and improve it if necessary.

- Research and Compare Lenders – Shop around for different lenders to find the best interest rates, fees, and repayment options.

- Calculate Costs and Break-Even Point – Factor in closing costs and estimate how long it will take to recover these expenses through savings.

- Gather Required Documents – Prepare financial documents such as tax returns, bank statements, and loan details for the application.

- Apply for the Refinance Loan – Submit your application with the chosen lender and undergo a credit check and potential home appraisal.

- Review Loan Offers and Terms – Carefully read the new loan terms to ensure they align with your financial goals.

- Close on the New Loan – Sign the final paperwork, pay closing costs if required, and transition from the old loan to the new one.

- Start Making Payments on Your New Loan – Set up payment reminders or automatic transfers to stay on track with your new loan.

Conclusion

Refinancing can be a powerful financial tool when used strategically, offering benefits such as lower interest rates, reduced monthly payments, and improved loan terms. However, it’s essential to carefully evaluate your financial situation, compare loan offers, and consider the costs associated with refinancing before making a decision. While refinancing can lead to long-term savings and greater financial flexibility, it may not always be the right move, especially if the costs outweigh the benefits. By understanding the refinancing process and aligning it with your financial goals, you can make an informed decision that helps you manage debt more effectively and improve your overall financial well-being.