Unexpected medical emergencies can have devastating financial consequences, even if you have health insurance. While standard health insurance helps cover medical bills, it doesn’t always account for lost income, long-term care, or other non-medical expenses that arise during a serious illness. This is where critical illness insurance comes in. Designed to provide a lump-sum payout upon diagnosis of a severe condition like cancer, heart attack, or stroke, critical illness insurance offers financial flexibility beyond traditional medical coverage. But how does it differ from standard health insurance, and who really needs it? This article breaks down the key differences, benefits, and considerations to help you determine if critical illness insurance is right for you.

What is Critical Illness Insurance?

Critical illness insurance is a specialized form of coverage designed to provide financial protection when you are diagnosed with a severe, life-threatening condition. Unlike standard health insurance, which reimburses medical expenses, critical illness insurance offers a lump-sum payout that can be used for any purpose, whether it’s covering out-of-pocket medical costs, paying rent or mortgage, or even funding daily living expenses. This policy typically covers serious conditions such as heart attack, stroke, cancer, kidney failure, and major organ transplants, though coverage varies by insurer. The primary goal of critical illness insurance is to ease the financial burden that comes with managing a major illness, allowing policyholders to focus on recovery without worrying about the impact on their finances.

What is Standard Health Insurance?

Standard health insurance is a comprehensive policy that helps cover the costs of medical care, including doctor visits, hospital stays, surgeries, medications, and preventive services. Unlike critical illness insurance, which provides a one-time lump-sum payout, standard health insurance works on a reimbursement or direct billing system, where the insurer covers eligible medical expenses either partially or in full, depending on the plan. Most health insurance policies include co-pays, deductibles, and out-of-pocket limits, ensuring that policyholders share some of the financial responsibility for their healthcare. Additionally, many health insurance plans cover a wide range of medical conditions and treatments, making them essential for managing routine and emergency healthcare needs. However, standard health insurance may not always cover non-medical expenses or lost income, which is where supplemental policies like critical illness insurance can provide additional financial support.

Key Differences between Critical Illness Insurance and Standard Health Insurance

While both critical illness insurance and standard health insurance provide financial protection against medical conditions, they serve different purposes. Standard health insurance covers a broad range of medical expenses, including hospitalizations, doctor visits, and prescriptions, reimbursing costs or paying providers directly. Critical illness insurance, on the other hand, provides a lump-sum payout upon diagnosis of a serious illness, giving policyholders the flexibility to use the funds as needed—whether for treatment, daily living expenses, or other financial obligations. Below is a detailed comparison of their key differences:

| Factor | Critical Illness Insurance | Standard Health Insurance |

| Coverage Scope | Covers specific life-threatening illnesses (e.g., cancer, stroke, heart attack) | Covers a wide range of medical conditions, including minor and major illnesses |

| Payout Type | Lump-sum cash payment upon diagnosis | Reimburses or directly pays medical expenses incurred |

| Usage of Funds | Can be used for any purpose (medical or non-medical expenses) | Can only be used for approved medical expenses |

| Number of Claims Allowed | Typically one-time payout per condition | Multiple claims allowed throughout the policy term |

| Policy Duration | Long-term policy, often renewed annually | Annual or multi-year policy, renewed as per insurer’s terms |

| Premium Cost | Generally lower than standard health insurance | Higher premiums due to broader coverage |

| Waiting Period | Usually 90 days from policy start; 30-90 days survival period after diagnosis | Generally 30 days for new policies; pre-existing conditions may have longer waiting periods |

| Pre-existing Conditions | Often excluded from coverage | Coverage depends on the insurer but may have waiting periods |

| Ideal For | People at high risk of critical illnesses, those seeking financial security beyond medical bills | General healthcare needs, preventive care, and hospitalization coverage |

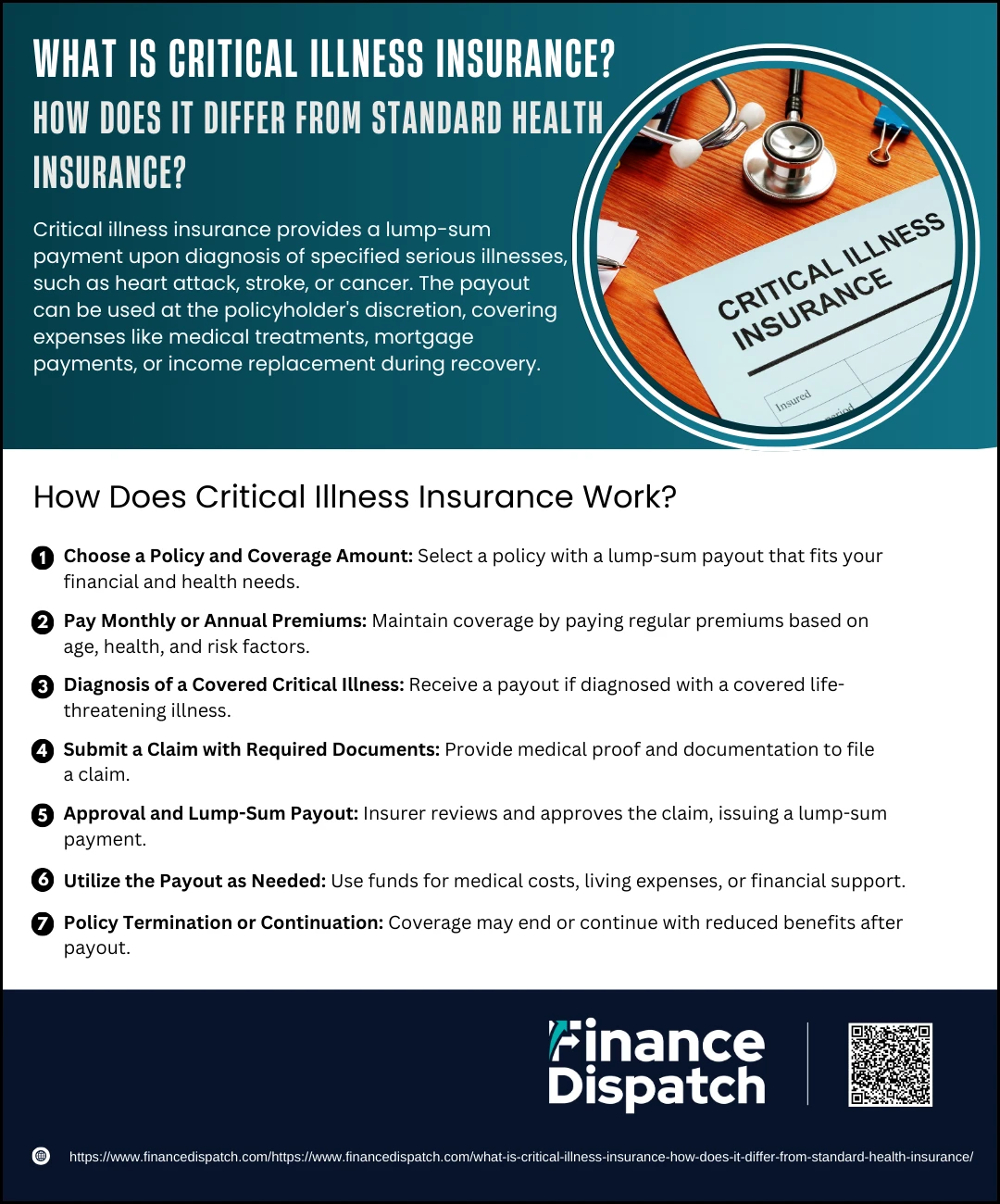

How Does Critical Illness Insurance Work?

How Does Critical Illness Insurance Work?

Critical illness insurance is designed to provide financial support when you are diagnosed with a life-threatening illness. Unlike traditional health insurance, which reimburses specific medical costs, this policy offers a one-time lump-sum payout upon diagnosis of a covered condition. The flexibility of this payout allows policyholders to use the funds for medical treatments, rehabilitation, mortgage payments, lost income, or any other expenses they may face during recovery. This type of insurance is especially beneficial for individuals who may struggle with the financial burden of prolonged treatment or time away from work.

The process of how critical illness insurance works can be broken down into the following steps:

1. Choose a Policy and Coverage Amount

When purchasing critical illness insurance, you need to choose a policy that aligns with your financial needs and health risks. The coverage amount, which determines the lump-sum payout, can range from a few thousand to hundreds of thousands of dollars. The more extensive the coverage, the higher the premium.

2. Pay Monthly or Annual Premiums

To maintain coverage, policyholders must pay regular premiums. These premiums are determined by factors such as age, health status, smoking habits, and family medical history. Generally, younger and healthier individuals receive lower premium rates.

3. Diagnosis of a Covered Critical Illness

If you are diagnosed with a critical illness listed in your policy, such as heart attack, cancer, stroke, or kidney failure, you become eligible to file a claim. Some policies include additional conditions, such as paralysis, coma, major organ transplants, and Alzheimer’s disease. However, pre-existing conditions and some early-stage illnesses may not be covered.

4. Submit a Claim with Required Documents

To initiate a claim, you must provide documentation such as medical reports, diagnostic test results, and a certification from a doctor confirming the diagnosis. Some insurers may require additional medical evaluations to validate the claim.

5. Approval and Lump-Sum Payout

Once the insurance provider reviews and approves the claim, a lump-sum payout is issued to the policyholder. The payout amount is pre-determined based on the coverage selected at the time of purchase. Unlike health insurance, which directly covers hospital bills, this payout is not restricted to medical expenses and can be used as needed.

6. Utilize the Payout as Needed

The policyholder has complete control over how to use the payout. It can cover:

- Medical expenses (hospital bills, medications, rehabilitation therapy).

- Household expenses (mortgage or rent, utility bills, childcare).

- Lost income due to the inability to work during treatment and recovery.

- Transportation and home modifications for accessibility if needed.

7. Policy Termination or Continuation

Depending on the policy type, the insurance may end after the payout or continue with reduced coverage. Some policies allow partial payouts for less severe conditions, while others terminate after the full sum has been disbursed.

Who Needs Critical Illness Insurance?

Life is unpredictable, and a serious illness can strike at any time, disrupting both health and finances. While standard health insurance covers medical treatments, it may not fully address the financial burden of lost income, rehabilitation, or daily living expenses. Critical illness insurance provides a lump-sum payout when diagnosed with a covered condition, offering financial relief during recovery. But is it necessary for everyone? Below are key groups of people who may benefit the most from critical illness coverage:

- Individuals with a Family History of Critical Illness

If diseases like cancer, heart disease, or stroke run in your family, your risk of developing these conditions may be higher, making this insurance a smart investment. - Sole Breadwinners

If your family relies on your income, a severe illness could leave them financially vulnerable. Critical illness insurance ensures they have the necessary financial support while you recover. - Self-Employed and Freelancers

Without employer-provided health benefits or sick leave, self-employed individuals may struggle with income loss during treatment. This policy provides a financial cushion during recovery. - People with High-Risk Lifestyles or Jobs

Those working in stressful, physically demanding, or hazardous jobs (e.g., firefighters, construction workers, pilots) are more likely to develop severe health issues over time. - Individuals Over 40 Years Old

The risk of critical illnesses increases with age, and healthcare costs rise accordingly. Having coverage in place before health issues arise can be financially beneficial. - Parents with Young Children

Raising children comes with significant financial responsibilities. If a critical illness affects your ability to work, this policy can help maintain stability for your family. - People with High Financial Obligations

Those with mortgages, car loans, or education expenses may struggle with payments if they become unable to work. A critical illness payout can help cover these costs. - Those Without Substantial Savings

If you don’t have a strong emergency fund to cover extended medical treatment and recovery, this insurance acts as a financial backup.

Pros and Cons of Critical Illness Insurance

Pros and Cons of Critical Illness Insurance

Critical illness insurance can be a valuable financial safety net, offering a lump-sum payout when diagnosed with a severe illness such as cancer, heart attack, or stroke. Unlike standard health insurance, which only covers medical expenses, critical illness insurance provides flexible financial support that can be used for non-medical costs like mortgage payments, household expenses, or income replacement. However, like any insurance policy, it comes with both advantages and drawbacks. Here’s a closer look at the pros and cons of critical illness insurance:

Pros of Critical Illness Insurance

1. Financial Security during Medical Emergencies

A major illness can lead to unexpected medical expenses, lost income, and financial instability. A lump-sum payout from critical illness insurance provides immediate funds to cover treatment, recovery, and daily living costs.

2. Flexibility in Fund Usage

Unlike health insurance, which directly covers medical expenses, critical illness insurance gives you full control over how to use the money. You can pay for treatments, medications, rehabilitation, or even non-medical costs like rent, groceries, or childcare.

3. Low Premiums Compared to Health Insurance

Critical illness insurance tends to be more affordable than full health insurance, making it an attractive option for those looking for financial protection without high monthly costs.

4. Covers High Treatment Costs

The cost of treating life-threatening illnesses such as cancer, stroke, or heart disease can be overwhelming. Even with health insurance, co-pays, deductibles, and uncovered treatments can add up. This policy helps bridge the financial gap.

5. Helps Replace Lost Income

Many people are unable to work while undergoing treatment for serious illnesses. The lump-sum payment acts as income replacement, helping you manage daily expenses while you focus on recovery.

6. Portable Coverage

Unlike employer-provided health insurance, critical illness policies are portable, meaning you can keep the coverage even if you switch jobs or retire.

7. Peace of Mind

The fear of financial ruin due to a severe illness can be stressful. Having critical illness insurance provides peace of mind, knowing you’ll have financial support if needed.

Cons of Critical Illness Insurance

1. Limited Coverage

Critical illness insurance only covers specific illnesses listed in the policy. If you develop a condition not included—such as early-stage cancer or chronic diseases like diabetes—you won’t receive a payout.

2. One-Time Payout

Unlike health insurance, which covers multiple treatments over time, critical illness insurance usually provides a single lump-sum payment. Once you receive the payout, the policy often ends, even if further medical expenses arise.

3. Pre-Existing Conditions May Be Excluded

If you have a pre-existing condition, insurers may exclude it from coverage or charge a higher premium, limiting the usefulness of the policy.

4. Waiting Periods Apply

Most policies include a waiting period (usually 90 days from the start of the policy) before coverage becomes active. Additionally, many policies have a survival period (typically 30–90 days after diagnosis) before you can claim benefits.

5. Premiums May Increase with Age

While initial premiums are low, they may increase as you age. This could make maintaining the policy expensive later in life when you are more likely to need coverage.

6. May Overlap with Existing Health and Disability Insurance

If you already have a comprehensive health or disability insurance policy, critical illness insurance might be redundant, adding unnecessary expenses to your budget.

7. Not a Replacement for Standard Health Insurance

Critical illness insurance does not cover routine medical expenses, hospital stays, or doctor visits. It should be seen as a supplemental policy, not a replacement for standard health insurance.

When Should You Consider Buying Critical Illness Insurance?

Deciding when to buy critical illness insurance depends on several personal and financial factors, including your health risks, financial obligations, and existing coverage. The best time to purchase a policy is when you are young and healthy, as premiums are lower, and there are fewer chances of exclusions due to pre-existing conditions. If you have a family history of serious illnesses such as heart disease, cancer, or stroke, getting coverage early can provide peace of mind and financial security. Additionally, those who are sole breadwinners, self-employed, or without employer-provided health benefits should consider buying a policy to protect against income loss if they become too ill to work. It’s also a wise choice for individuals with large financial obligations like mortgages, children’s education expenses, or debts, as a lump-sum payout can help cover these costs during recovery. If your standard health insurance has high deductibles or limited coverage for long-term treatments, critical illness insurance can act as a financial safety net to prevent out-of-pocket strain. Ultimately, purchasing a policy before a serious illness arises ensures that you are financially prepared for unexpected medical challenges.

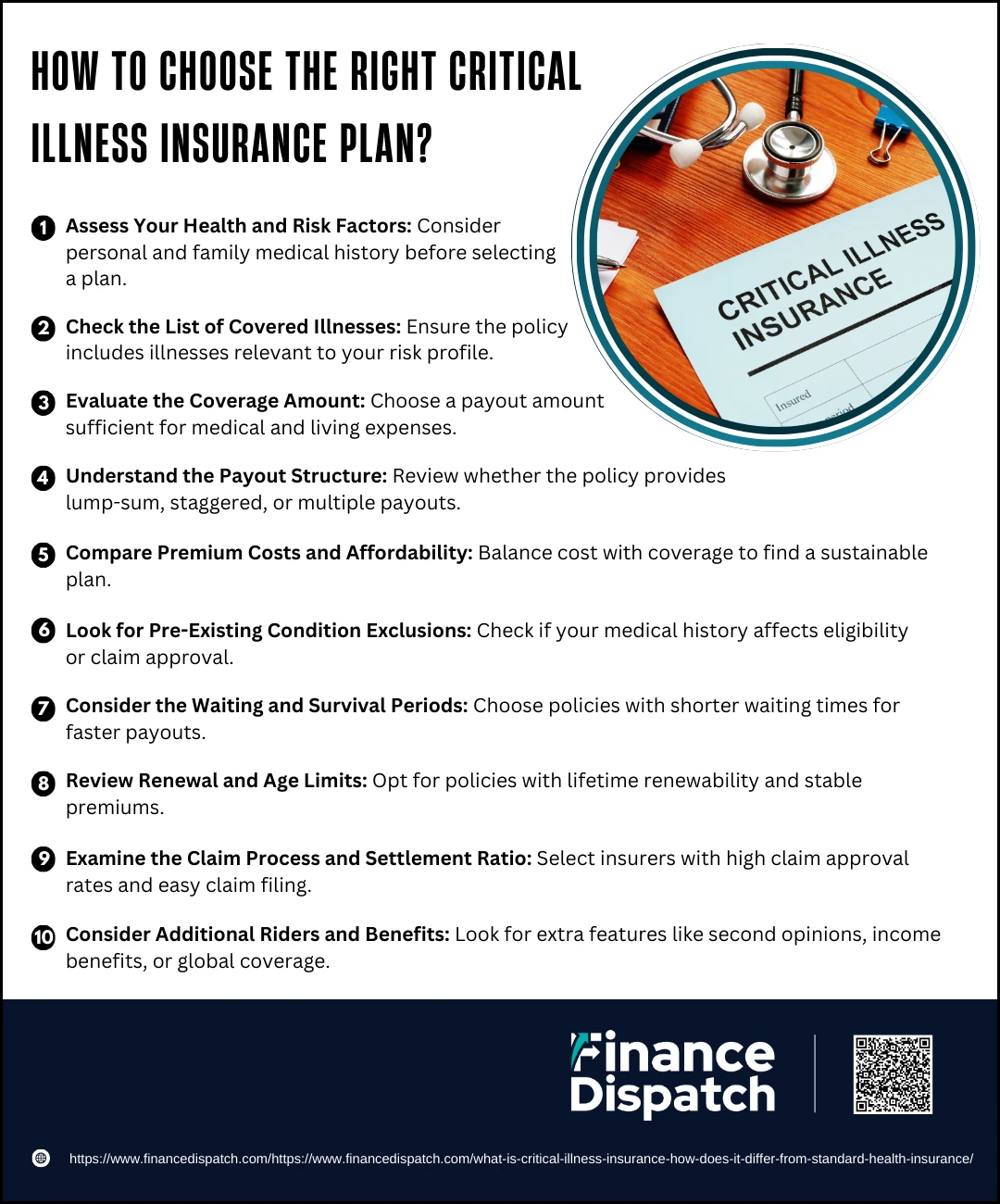

How to Choose the Right Critical Illness Insurance Plan?

How to Choose the Right Critical Illness Insurance Plan?

Choosing the right critical illness insurance plan is crucial for ensuring financial security in the event of a serious illness. Since these policies vary in coverage, exclusions, payout structures, and costs, it’s important to carefully evaluate your options before making a decision. A well-selected plan should provide adequate financial protection, ensuring that you can cover medical expenses, lost income, and other essential costs without financial strain. Whether you’re purchasing a policy for yourself or your family, here are the key factors to consider to ensure you make an informed decision.

1. Assess Your Health and Risk Factors

Start by evaluating your personal and family medical history. If you have a family history of serious illnesses like heart disease, stroke, or cancer, you may be at higher risk and should opt for a plan that covers these conditions extensively. Additionally, consider lifestyle factors such as stress levels, smoking, diet, and work environment, as they can increase your risk of developing critical illnesses.

2. Check the List of Covered Illnesses

Not all critical illness insurance plans cover the same conditions. Some policies include only a handful of major illnesses like heart attack, stroke, and cancer, while others provide coverage for a broader range of diseases, including kidney failure, organ transplants, paralysis, and neurological disorders. Carefully review the list of covered illnesses to ensure the policy aligns with your specific health risks.

3. Evaluate the Coverage Amount

The payout from your critical illness insurance should be enough to cover medical expenses, lost income, and daily living costs. Experts recommend choosing a sum assured that can cover 2-5 years of expenses, including hospital bills, mortgage payments, and other financial obligations. If you are the sole breadwinner, opt for a higher coverage amount to maintain financial stability for your family.

4. Understand the Payout Structure

Different policies have different payout structures. Some provide a full lump-sum payment upon diagnosis, while others offer staggered or partial payments based on the severity of the illness. Some policies also allow multiple claims for different illnesses over time. Choose a payout structure that offers financial flexibility and meets your long-term needs.

5. Compare Premium Costs and Affordability

The cost of premiums varies depending on age, health status, smoking habits, and policy coverage. While lower premiums may seem attractive, they might offer limited coverage or lower payouts. It’s essential to balance affordability with adequate coverage to ensure long-term sustainability without unnecessary financial strain.

6. Look for Pre-Existing Condition Exclusions

Most insurance providers exclude pre-existing medical conditions or impose long waiting periods before coverage applies. If you already have a medical condition, check whether the policy excludes it entirely or covers it after a waiting period. Understanding these exclusions ensures you won’t face unexpected claim denials when you need coverage the most.

7. Consider the Waiting and Survival Periods

Critical illness policies often have a waiting period (usually 90 days) from the time of purchase before claims can be made. Additionally, many policies include a survival period (typically 30-90 days) after diagnosis before the payout is processed. Opt for a policy with shorter waiting and survival periods to ensure quicker financial support.

8. Review Renewal and Age Limits

Some insurance policies limit renewability or reduce coverage after a certain age (e.g., 65 or 70 years). If you are buying a policy at a young age, choose a plan with lifetime renewability to ensure coverage continues as you age. Avoid plans that significantly reduce benefits or increase premiums drastically over time.

9. Examine the Claim Process and Settlement Ratio

A seamless and efficient claim process is critical during medical emergencies. Research the claim settlement ratio of different insurance providers, which indicates the percentage of claims they successfully approve. Companies with higher claim settlement ratios are generally more reliable in honoring payouts. Also, check how easy it is to file a claim—some insurers require excessive paperwork, while others offer hassle-free digital claim processing.

10. Consider Additional Riders and Benefits

Some insurance plans offer optional riders that can enhance your coverage, such as:

- Second medical opinion: Allows access to expert consultation from global specialists.

- Air ambulance cover: Helps cover transportation costs for emergency treatment.

- Global coverage: Extends coverage for treatment outside your home country.

- Premium waiver benefit: Waives future premiums if diagnosed with a covered illness.

- Income benefit rider: Provides an additional income stream if unable to work.

If these riders align with your needs, consider adding them to strengthen your policy.

Conclusion

Critical illness insurance serves as a financial safety net for individuals facing life-threatening health conditions. Unlike standard health insurance, which covers medical expenses, this policy provides a lump-sum payout that can be used for treatment costs, income replacement, household expenses, and other financial obligations. Choosing the right plan requires careful evaluation of factors such as covered illnesses, payout structure, waiting periods, exclusions, and affordability. While not everyone may need this type of coverage, it can be particularly beneficial for those with a family history of critical illnesses, sole breadwinners, self-employed individuals, or people with significant financial commitments. Ultimately, investing in critical illness insurance can provide peace of mind, ensuring that you and your loved ones remain financially secure during difficult times. Before purchasing a policy, it’s essential to compare options, understand the terms, and choose a plan that best fits your health risks and financial needs.