In today’s fast-paced world, managing your finances efficiently is more important than ever, and a checking account serves as the foundation for financial organization. Whether it’s paying bills, receiving your paycheck via direct deposit, or making everyday purchases with a debit card, a checking account offers unmatched convenience, security, and flexibility. Unlike savings accounts, which are designed for long-term storage and growth of funds, checking accounts prioritize accessibility, allowing you to manage your money seamlessly. From automated bill payments to mobile check deposits, these accounts are equipped with tools that simplify your daily financial tasks. In this article, we’ll explore what a checking account is, how it works, its essential features, and why it remains a cornerstone of personal finance management.

What is a Checking Account?

A checking account is a type of bank account designed for managing everyday financial transactions with ease and convenience. It serves as a secure place to deposit money, receive paychecks, and make payments for bills, groceries, and other expenses using checks, debit cards, or online transfers. Unlike savings accounts, checking accounts are not primarily intended for long-term savings and typically offer little to no interest on the balance. However, they excel in accessibility, allowing unlimited deposits and withdrawals, often without restrictions. With features such as online banking, mobile banking, direct deposit, and overdraft protection, checking accounts provide tools to streamline daily money management. Whether you’re paying rent, buying groceries, or setting up recurring payments, a checking account acts as the financial hub for handling your day-to-day monetary needs.

Why is a Checking Account Essential for Daily Transactions?

In today’s fast-paced and digital-driven world, a checking account has become a fundamental financial tool for managing daily expenses and transactions. It provides a seamless, secure, and efficient way to handle financial activities such as paying bills, receiving salaries, transferring funds, and making purchases through debit cards or online banking. Unlike savings accounts, which focus on growing your funds, checking accounts are specifically designed for frequent access and easy money management. With advanced features like mobile banking, direct deposits, and overdraft protection, checking accounts simplify daily financial responsibilities and contribute to better money management. Below are detailed explanations of the key reasons why a checking account is essential for daily transactions.

1. Direct Deposit for Instant Access to Funds

Direct deposit allows your paycheck, government benefits, or other regular income to be electronically deposited directly into your checking account. This eliminates the need for physical checks, reduces the risk of loss or theft, and ensures your funds are available quickly, often on the same day as payday. Many employers and government agencies prefer direct deposits as they are reliable, faster, and environmentally friendly. Additionally, some banks offer perks, such as waiving maintenance fees, if you set up direct deposit.

2. Convenient Bill Payments

Checking accounts simplify the process of paying bills, whether they’re for utilities, rent, mortgage, or subscription services. You can set up automatic payments or use online bill pay to schedule recurring payments. This ensures you never miss a due date, helping you avoid late fees and maintain a good payment history. Furthermore, many banks provide reminders and alerts for upcoming payments, allowing you to stay on top of your financial commitments.

3. Debit Card Transactions

A debit card, linked to your checking account, allows you to make purchases both online and in physical stores without carrying cash. Debit cards also provide easy access to cash at ATMs. Many debit cards come with zero-liability protection, meaning you won’t be held responsible for unauthorized transactions if you report them promptly. This makes debit cards not only convenient but also a safer option for daily expenses.

4. Easy Access to ATMs

Checking accounts provide access to Automated Teller Machines (ATMs) for quick and convenient withdrawals, deposits, or balance inquiries. Most banks have extensive ATM networks that allow fee-free transactions within their network. With ATMs available in convenient locations such as grocery stores, malls, and airports, you can manage your cash needs anytime, day or night.

5. Financial Tracking and Budgeting

Checking accounts offer robust tools for tracking spending and budgeting. With monthly statements, online banking dashboards, and mobile apps, you can review your transactions, monitor your spending habits, and set financial goals. Many banks also provide spending categorization features, helping you see where your money goes and make adjustments to your budget if needed.

6. Overdraft Protection

Overdraft protection is a feature that prevents your transactions from being declined due to insufficient funds in your checking account. If you spend more than what’s available, the bank may automatically transfer money from a linked savings account, credit card, or overdraft line of credit to cover the difference. While some banks charge fees for this service, it can save you from hefty penalties, returned check fees, and the embarrassment of declined payments.

7. Enhanced Security and Fraud Protection

Checking accounts come with advanced security measures to protect your funds. These include encryption, two-factor authentication, and fraud monitoring systems. Additionally, most checking accounts are insured by the FDIC (Federal Deposit Insurance Corporation) or NCUA (National Credit Union Administration) up to $250,000 per depositor. This ensures your money remains safe even in the unlikely event of a bank failure.

8. Flexibility in Fund Transfers

Checking accounts allow for easy fund transfers between accounts, whether within the same bank or across different institutions. You can also transfer money to friends and family using peer-to-peer payment apps like Zelle, Venmo, or PayPal, which are often linked to checking accounts. This flexibility makes it easier to handle shared expenses, split bills, or send emergency funds when needed.

9. Proof of Financial Stability

Having a checking account provides a documented history of your financial responsibility, which can be valuable when applying for loans, mortgages, or rental agreements. Banks and lenders often review your account activity to assess your financial reliability. Regular use of your checking account demonstrates stability and a pattern of responsible money management, which can improve your creditworthiness.

10. Reduces the Need for Cash

Carrying large amounts of cash can be risky and inconvenient. A checking account allows you to make secure electronic transactions via debit cards, mobile banking, or online payments. Many retailers and service providers prefer digital payments, and features like contactless payments and mobile wallet integration (e.g., Apple Pay, Google Pay) make transactions even faster and safer.

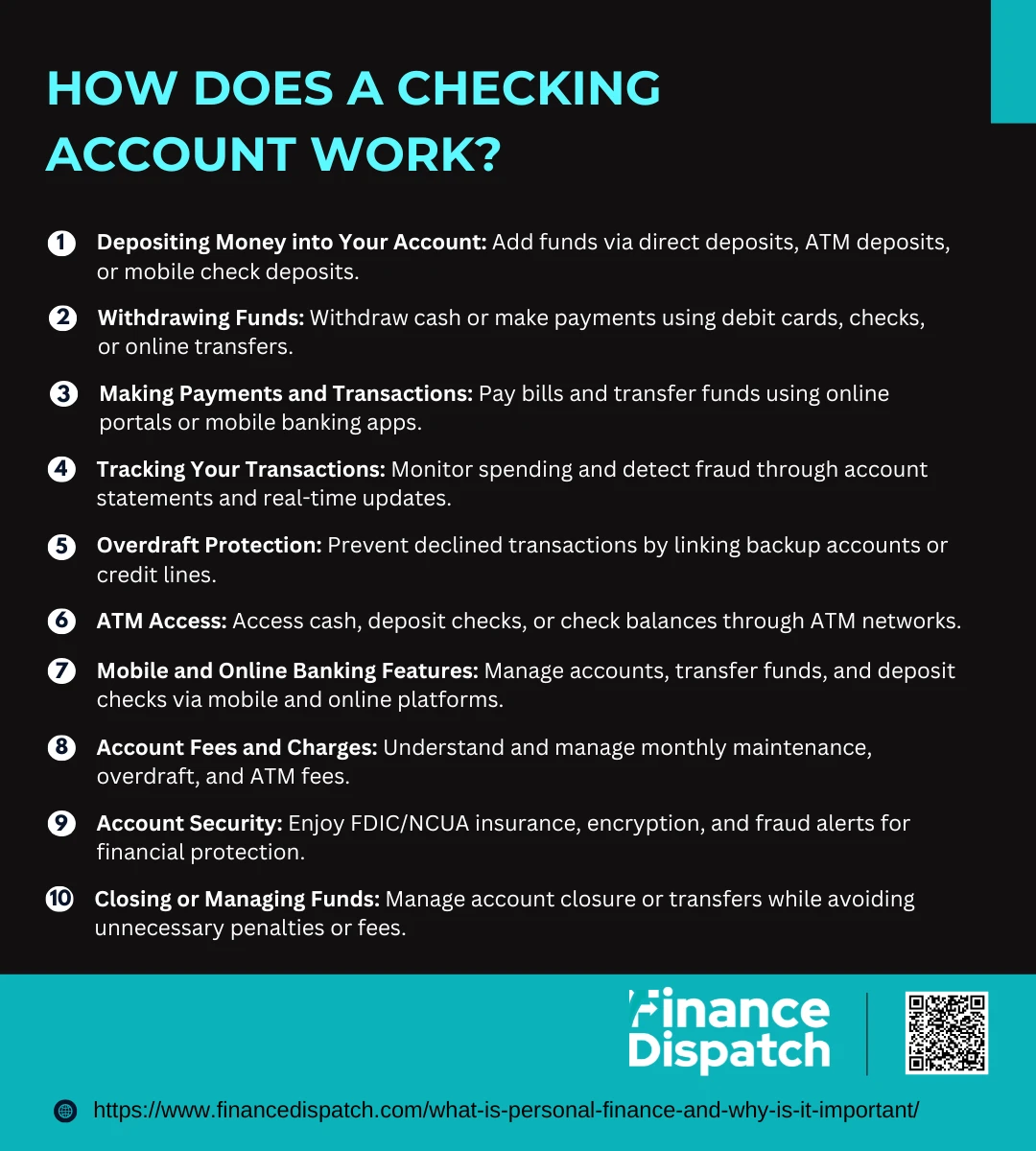

How Does a Checking Account Work?

A checking account serves as a financial hub for managing your everyday money transactions, offering a secure and efficient way to handle deposits, withdrawals, and payments. Whether you’re paying bills, making purchases with a debit card, or setting up direct deposits for your salary, a checking account acts as a versatile tool for seamless financial management. It allows you to access your funds conveniently through checks, ATMs, mobile banking apps, or online platforms. Unlike savings accounts, which focus on long-term storage and interest accumulation, checking accounts are designed for frequent transactions. Below, we’ll break down how a checking account works, step-by-step, to give you a clearer understanding of its functionality.

1. Depositing Money into Your Account

Money can be deposited into a checking account through several methods, including direct deposits from your employer, cash or check deposits at ATMs or bank branches, and mobile check deposits via your banking app. Direct deposits are one of the most common and efficient ways to receive funds, ensuring immediate access without requiring physical visits to a bank.

2. Withdrawing Funds

Funds can be withdrawn from your checking account using debit cards at ATMs, writing paper checks, or transferring money electronically through online banking services. Many banks also allow cash withdrawals directly from bank tellers at branches. Debit cards provide an added layer of convenience for everyday spending, eliminating the need to carry large amounts of cash.

3. Making Payments and Transactions

Checking accounts simplify paying bills and making purchases. You can set up automatic bill payments for recurring expenses like utilities, rent, and loan payments. Online banking portals and mobile apps allow you to make one-time payments, transfer funds, or send money through peer-to-peer payment platforms such as Zelle or Venmo.

4. Tracking Your Transactions

Every activity in your checking account—deposits, withdrawals, transfers, and payments—is recorded and reflected in your monthly bank statement or through real-time updates on your mobile banking app. This tracking feature helps you monitor your spending habits, budget effectively, and quickly detect any fraudulent activity or errors.

5. Overdraft Protection

If you attempt to make a payment or withdrawal that exceeds your account balance, overdraft protection prevents the transaction from being declined. The bank may cover the shortfall by transferring funds from a linked savings account or offering a temporary line of credit. However, overdraft protection may come with fees, so it’s essential to monitor your account balance regularly.

6. ATM Access

Checking accounts typically come with access to a network of Automated Teller Machines (ATMs) for cash withdrawals, check deposits, or balance inquiries. While most banks offer free ATM transactions within their network, using an out-of-network ATM may incur additional fees.

7. Mobile and Online Banking Features

Modern checking accounts offer robust digital banking tools. Mobile apps and online banking portals allow account holders to check balances, transfer funds, deposit checks remotely, and set account alerts. These tools ensure that managing your money is quick, convenient, and available at your fingertips.

8. Account Fees and Charges

Some checking accounts may charge monthly maintenance fees, overdraft fees, or ATM usage fees. However, many banks offer fee waivers if specific conditions are met, such as maintaining a minimum balance, setting up direct deposits, or using online banking services regularly.

9. Account Security

Checking accounts are protected by encryption technologies and often come with FDIC (Federal Deposit Insurance Corporation) or NCUA (National Credit Union Administration) insurance, safeguarding your deposits up to $250,000. Additional features like fraud alerts, two-factor authentication, and transaction monitoring further enhance account security.

10. Closing or Managing Funds

If you decide to close your checking account, you’ll need to withdraw or transfer the remaining balance. Banks may charge a closing fee if the account has been open for a short duration. Managing a checking account effectively involves avoiding unnecessary fees, keeping track of transactions, and ensuring sufficient funds are always available.

Key Features of a Checking Account

A checking account is a fundamental financial tool designed for managing everyday transactions with ease and efficiency. It serves as the hub for receiving paychecks, paying bills, transferring funds, and making purchases. Unlike savings accounts, checking accounts prioritize accessibility and convenience, offering features like debit cards, online banking, and mobile deposits to simplify financial management. Whether you’re handling personal expenses or managing shared finances, a checking account provides the tools and security needed for seamless money management. Below are the key features of a checking account, along with brief descriptions of their benefits.

- Debit Card Access: Easily make purchases and withdraw cash using a debit card linked to your checking account.

- Direct Deposit: Receive your salary or government benefits directly into your account without delays.

- Online and Mobile Banking: Manage your account, check balances, and transfer funds anytime via digital platforms.

- Bill Payment Services: Set up one-time or recurring bill payments directly from your account.

- ATM Access: Withdraw cash or make deposits at ATMs within your bank’s network.

- Overdraft Protection: Prevent declined transactions or bounced checks by linking a backup account or credit line.

- Account Statements: Receive detailed monthly account statements to track spending and deposits.

- Check-Writing Privileges: Write checks for payments when electronic options aren’t available.

- Fraud Protection: Enjoy real-time monitoring and alerts for suspicious account activity.

- FDIC/NCUA Insurance: Your funds are insured up to $250,000, ensuring safety in case of bank failure.

- Spending and Budgeting Tools: Access tools to track spending and create budgets through mobile apps.

- Flexible Fund Transfers: Transfer money seamlessly between accounts or peer-to-peer apps.

- Account Alerts: Set up notifications for low balances, large transactions, or suspicious activities.

- Minimal Balance Requirements: Many accounts offer low or no minimum balance requirements.

- Mobile Check Deposit: Deposit checks remotely using your bank’s mobile app.

Benefits of Having a Checking Account

A checking account is more than just a place to store your money—it’s a versatile financial tool designed to simplify your day-to-day transactions, offer financial security, and promote better money management habits. Whether you’re receiving your paycheck, paying bills, or transferring funds, a checking account provides unmatched convenience and accessibility. It serves as the foundation for modern financial management, enabling users to handle their finances with efficiency and confidence. With features like direct deposit, online banking, and debit card access, checking accounts are essential for anyone looking to streamline their personal or business finances. Below, we’ll explore the key benefits of having a checking account in greater detail.

1. Convenient Access to Funds

A checking account offers easy access to your money through various channels, including debit cards, ATMs, mobile banking apps, and online banking portals. You can withdraw cash, make purchases, or transfer funds without restrictions, ensuring that your money is always within reach whenever you need it.

2. Direct Deposit

With direct deposit, your salary, government benefits, or other regular payments can be electronically transferred directly into your checking account. This eliminates the hassle of paper checks, reduces the risk of theft or loss, and gives you immediate access to your funds on payday.

3. Secure Way to Store Money

Funds in a checking account are protected by FDIC (Federal Deposit Insurance Corporation) or NCUA (National Credit Union Administration) insurance, covering up to $250,000 per depositor, per institution. This provides peace of mind, knowing your money is secure even if the bank faces financial troubles.

4. Simplified Bill Payments

With a checking account, you can set up automatic payments for recurring bills such as rent, utilities, loans, and subscriptions. This ensures payments are made on time, avoiding late fees and protecting your credit score. Online bill payment services also allow you to track your expenses more efficiently.

5. Easy Fund Transfers

Checking accounts allow for seamless transfers between accounts, both within the same bank and across different financial institutions. You can also link your account to peer-to-peer (P2P) payment apps like Venmo, Zelle, or PayPal, making it easy to split bills, pay friends, or transfer money in seconds.

6. Overdraft Protection

Many banks offer overdraft protection, which covers transactions even when your account lacks sufficient funds. This feature prevents declined payments, bounced checks, and hefty overdraft fees by automatically transferring funds from a linked savings account or line of credit.

7. Mobile and Online Banking

Modern checking accounts offer advanced online and mobile banking features. With these tools, you can check balances, deposit checks remotely, set up account alerts, transfer funds, and make payments—all from your smartphone or computer. This ensures 24/7 access to your account, no matter where you are.

8. Financial Tracking and Budgeting Tools

Checking accounts often come with built-in financial tracking tools through online and mobile banking platforms. These tools categorize your expenses, generate monthly statements, and offer insights into your spending habits, helping you create and stick to a budget.

9. Debit Card Benefits

A debit card linked to your checking account allows you to make secure payments online and in-store, as well as withdraw cash from ATMs. Many debit cards come with additional perks, such as cashback rewards, fraud protection, and zero-liability coverage for unauthorized transactions.

10. Proof of Financial Stability

A checking account serves as a financial record that demonstrates your ability to manage money responsibly. This can be helpful when applying for loans, credit cards, or even rental agreements, as it shows lenders and landlords that you have a stable financial history.

11. Fraud Protection and Alerts

Banks provide robust fraud protection services for checking accounts, including transaction alerts, two-factor authentication, and real-time monitoring for suspicious activities. These measures help detect and prevent unauthorized transactions, ensuring your money remains safe.

12. Access to Additional Banking Services

Having a checking account often opens the door to other financial products, such as savings accounts, certificates of deposit (CDs), and personal loans. Some banks also offer discounts on financial products and special rewards for checking account holders.

13. Flexibility for Large Payments

While digital payments dominate, checks still play a role in handling large payments, such as rent or tuition. A checking account allows you to write checks, providing flexibility when electronic transfers aren’t an option.

14. Builds Financial Discipline

Using a checking account regularly promotes financial discipline by encouraging you to track your expenses, monitor balances, and avoid unnecessary fees. Regular account monitoring helps you stay on budget and make informed financial decisions.

15. Reduces Reliance on Cash

Carrying large amounts of cash is risky and impractical. A checking account reduces this need by enabling secure electronic payments through debit cards, mobile banking apps, and online platforms. Digital payments also offer better tracking and accountability.

16. Emergency Fund Access

In case of emergencies, having funds readily available in your checking account can be a lifesaver. Unlike savings accounts, which may have withdrawal restrictions, checking accounts provide immediate access to your money when you need it most.

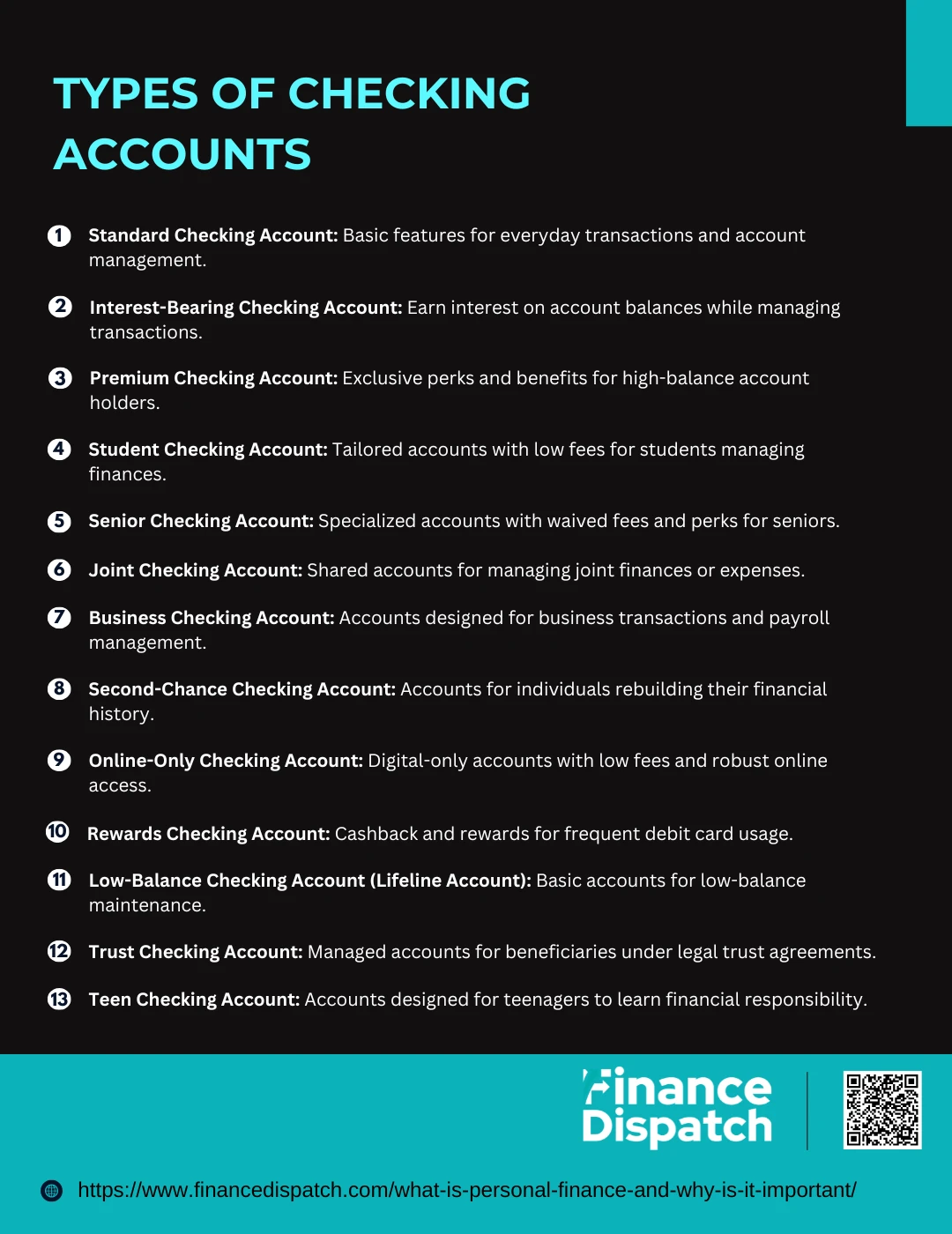

Types of Checking Accounts

Types of Checking Accounts

A checking account is an essential financial tool designed to manage everyday transactions, from paying bills and receiving direct deposits to making purchases and transferring funds. However, not all checking accounts are the same. Different types of checking accounts cater to specific financial needs, lifestyles, and goals. Whether you’re a student, a business owner, or someone looking for premium banking services, there’s a checking account tailored for you. Below, we’ll explore the most common types of checking accounts, along with their unique features and benefits.

1. Standard Checking Account

A standard checking account is the most common type, offering basic features such as debit card access, check-writing privileges, and online banking. It’s ideal for everyday transactions, and while some accounts may have monthly maintenance fees, these are often waived if specific requirements, such as a minimum balance or direct deposit, are met.

2. Interest-Bearing Checking Account

This type of checking account allows you to earn interest on your balance while still enjoying the convenience of everyday banking. Interest rates are usually low compared to savings accounts, and there may be minimum balance requirements to qualify for interest earnings.

2. Premium Checking Account

Designed for customers who maintain a high account balance, premium checking accounts offer additional benefits such as higher interest rates, waived fees, free checks, and access to financial advice. These accounts often come with exclusive perks but may have steep minimum balance requirements.

3. Student Checking Account

Student checking accounts are tailored for high school and college students, offering features such as low or no monthly fees, no minimum balance requirements, and free online banking. These accounts often come with financial education resources to help students learn money management skills.

4. Senior Checking Account

Targeted at individuals typically aged 55 and older, senior checking accounts often include waived fees, free checks, and discounts on banking services. These accounts are designed to accommodate the unique financial needs of retirees and seniors.

5. Joint Checking Account

A joint checking account is shared between two or more individuals, often spouses, partners, or family members. It allows multiple account holders to deposit, withdraw, and manage funds, making it ideal for managing shared expenses such as rent, utilities, or groceries.

6. Business Checking Account

Business checking accounts are designed specifically for small businesses, entrepreneurs, and large corporations. They offer features like higher transaction limits, payroll processing tools, and detailed expense tracking. These accounts may require business documentation during the application process.

7. Second-Chance Checking Account

For individuals who have a history of bounced checks, overdrafts, or closed accounts, second-chance checking accounts offer a fresh start. While these accounts may have higher fees or limited features, they provide an opportunity to rebuild financial trust with banks.

8. Online-Only Checking Account

Digital banks and fintech institutions offer online-only checking accounts, providing higher interest rates, lower fees, and 24/7 online banking access. However, these accounts usually lack physical branches, requiring customers to handle all banking activities digitally.

9. Rewards Checking Account

Some checking accounts offer cashback rewards, discounts, or perks for using your debit card or meeting certain spending criteria. These accounts are ideal for individuals who frequently use their debit cards for purchases.

10. Low-Balance Checking Account (Lifeline Account)

Also known as lifeline checking accounts, these are designed for individuals who cannot maintain a significant balance. They usually come with minimal fees and basic banking services, though they may have restrictions on the number of transactions allowed per month.

11. Trust Checking Account

Managed by a trustee, these accounts are used to hold and manage funds for beneficiaries according to the terms of a legal trust agreement. They are commonly used for estate planning and wealth management.

12. Teen Checking Account

A teen checking account is designed for teenagers to help them learn about budgeting, saving, and responsible money management. These accounts often require a parent or guardian as a co-owner and come with spending limits.

Common Fees Associated with Checking Accounts

While checking accounts offer convenience, flexibility, and essential tools for managing day-to-day finances, they often come with a variety of fees. These fees can add up quickly if you’re not aware of them or don’t manage your account carefully. From monthly maintenance charges to overdraft penalties, banks often impose these fees as part of their account services. However, many of these costs can be avoided by understanding their triggers and following good financial habits. Below are the most common fees associated with checking accounts, along with a brief explanation of each.

- Monthly Maintenance Fee: A recurring charge for account upkeep, often waived if specific requirements, like maintaining a minimum balance, are met.

- Overdraft Fee: Charged when you spend more money than what’s available in your account, covering the negative balance temporarily.

- Non-Sufficient Funds (NSF) Fee: Applied when a transaction is declined due to insufficient funds, usually for checks or scheduled payments.

- ATM Fees: Incurred when using an out-of-network ATM for cash withdrawals or balance inquiries.

- Foreign Transaction Fee: A fee charged for purchases or withdrawals made in a foreign currency or outside your bank’s network.

- Paper Statement Fee: Charged if you opt for paper account statements instead of electronic versions.

- Stop Payment Fee: Applied when you request the bank to stop processing a specific check or scheduled payment.

- Wire Transfer Fee: Charged for transferring funds electronically, with higher fees often for international transfers.

- Early Account Closure Fee: Imposed if you close your account shortly after opening, typically within 90 to 180 days.

- Returned Deposit Fee: Charged when a check you deposit bounces due to insufficient funds in the payer’s account.

- Inactivity Fee: Applied when an account remains dormant or inactive for an extended period, usually six months or more.

- Account Research Fee: A fee charged for extensive account investigations, such as locating old statements or resolving disputes.

- Check Printing Fee: Banks may charge for ordering personalized checks for your account.

- Excess Transaction Fee: Some accounts limit monthly transactions, and exceeding this limit incurs a fee.

- Debit Card Replacement Fee: Charged for replacing lost, stolen, or damaged debit cards.

Differences between Checking and Savings Accounts

When it comes to managing your money, checking accounts and savings accounts serve distinct purposes. A checking account is primarily designed for frequent transactions, such as paying bills, making purchases, and receiving direct deposits. It offers easy access to your funds through debit cards, checks, and online transfers. On the other hand, a savings account is built for long-term financial goals, encouraging users to save money while earning interest on their balance. While both accounts are essential financial tools, they cater to different needs and have unique features. Below is a detailed comparison of checking and savings accounts to help you understand their differences.

| Feature | Checking Account | Savings Account |

| Primary Purpose | Everyday transactions and bill payments | Long-term savings and financial growth |

| Accessibility | High – via debit cards, checks, ATMs, and online transfers | Limited – withdrawals are restricted to encourage saving |

| Interest Earnings | Usually minimal or none | Typically earns interest; higher rates for high-yield accounts |

| Withdrawal Limits | Unlimited withdrawals | May have monthly withdrawal limits (e.g., six per month) |

| Account Fees | Possible fees for maintenance, overdrafts, and ATM usage | Fewer fees, but may include minimum balance or withdrawal penalties |

| Minimum Balance Requirements | Often low or none | Usually required to avoid fees or earn higher interest |

| Overdraft Protection | Commonly available | Not available – withdrawals are usually limited to account balance |

| Debit Card Access | Yes, included with most accounts | Rarely provided; often limited to ATM cards |

| Direct Deposits | Commonly used for salaries and benefits | Less common; funds are usually transferred from checking accounts |

| Account Statements | Detailed monthly statements showing transactions | Statements focus on deposits, withdrawals, and interest earned |

| Best For | Managing daily expenses and recurring payments | Building an emergency fund or achieving financial goals |

How to Choose the Right Checking Account

Choosing the right checking account is a crucial step in managing your finances effectively. With various options available, each tailored to different needs and lifestyles, it’s essential to understand what features and benefits align with your financial habits. Whether you’re a student looking for low fees, a professional seeking premium perks, or someone who prefers online banking, the right checking account can make everyday financial tasks more manageable and cost-effective. Below are key factors to consider when selecting the ideal checking account for your needs.

- Monthly Maintenance Fees: Look for accounts with low or no monthly fees, or ensure they can be waived with conditions like direct deposits or minimum balances.

- Minimum Balance Requirements: Check if the account requires you to maintain a minimum balance to avoid penalties or qualify for perks.

- ATM Access and Fees: Consider accounts with fee-free access to a wide network of ATMs to avoid extra charges.

- Overdraft Protection: Look for accounts offering overdraft protection to prevent declined transactions or hefty fees.

- Online and Mobile Banking Features: Ensure the account offers robust online and mobile banking tools for convenient account management.

- Interest Earnings: If earning interest is important to you, opt for an interest-bearing checking account with competitive rates.

- Account Accessibility: Choose an account that offers multiple access points, including branches, ATMs, and digital platforms.

- Direct Deposit Benefits: Some accounts offer fee waivers or bonuses when you set up direct deposit.

- Customer Service Quality: Look for a bank with reliable customer support, whether online, over the phone, or in-branch.

- Account Fees Transparency: Review all potential fees, including ATM fees, foreign transaction fees, and overdraft charges.

- Rewards and Incentives: Some checking accounts offer cashback rewards or sign-up bonuses for new customers.

- Transaction Limits: Ensure the account fits your needs if it imposes limits on the number of transactions per month.

- Joint or Specialized Accounts: If needed, explore options for joint accounts, student accounts, or senior checking accounts.

- Security and Fraud Protection: Prioritize accounts with advanced security features like encryption, fraud alerts, and two-factor authentication.

- Bank Reputation and Reliability: Research the bank’s reputation for stability, customer service, and user reviews.

Conclusion

Choosing the right checking account is a fundamental step in managing your finances efficiently and avoiding unnecessary fees. With a variety of options available, from basic accounts with no monthly fees to premium accounts offering exclusive perks, it’s essential to evaluate your financial habits, needs, and long-term goals. Whether you’re looking for seamless online banking, overdraft protection, or cashback rewards, the ideal checking account should align with your lifestyle and offer flexibility for your day-to-day transactions. By carefully comparing features such as fees, ATM access, minimum balance requirements, and customer support, you can make an informed decision that simplifies your financial life. A well-chosen checking account is not just a financial tool—it’s the foundation for building a stable and stress-free banking experience.