Life has a way of throwing curveballs when you least expect them—an unexpected medical bill, a sudden job loss, or a car repair that just can’t wait. These surprises can quickly disrupt your financial balance, especially if you’re unprepared. That’s where an emergency fund comes in. More than just savings, an emergency fund acts as a financial safety net, providing you with the resources and confidence to navigate life’s uncertainties without falling into debt or derailing your long-term goals. In this article, we’ll explore what an emergency fund is, why it’s essential for your financial well-being, and how you can start building one—no matter where you are in your financial journey.

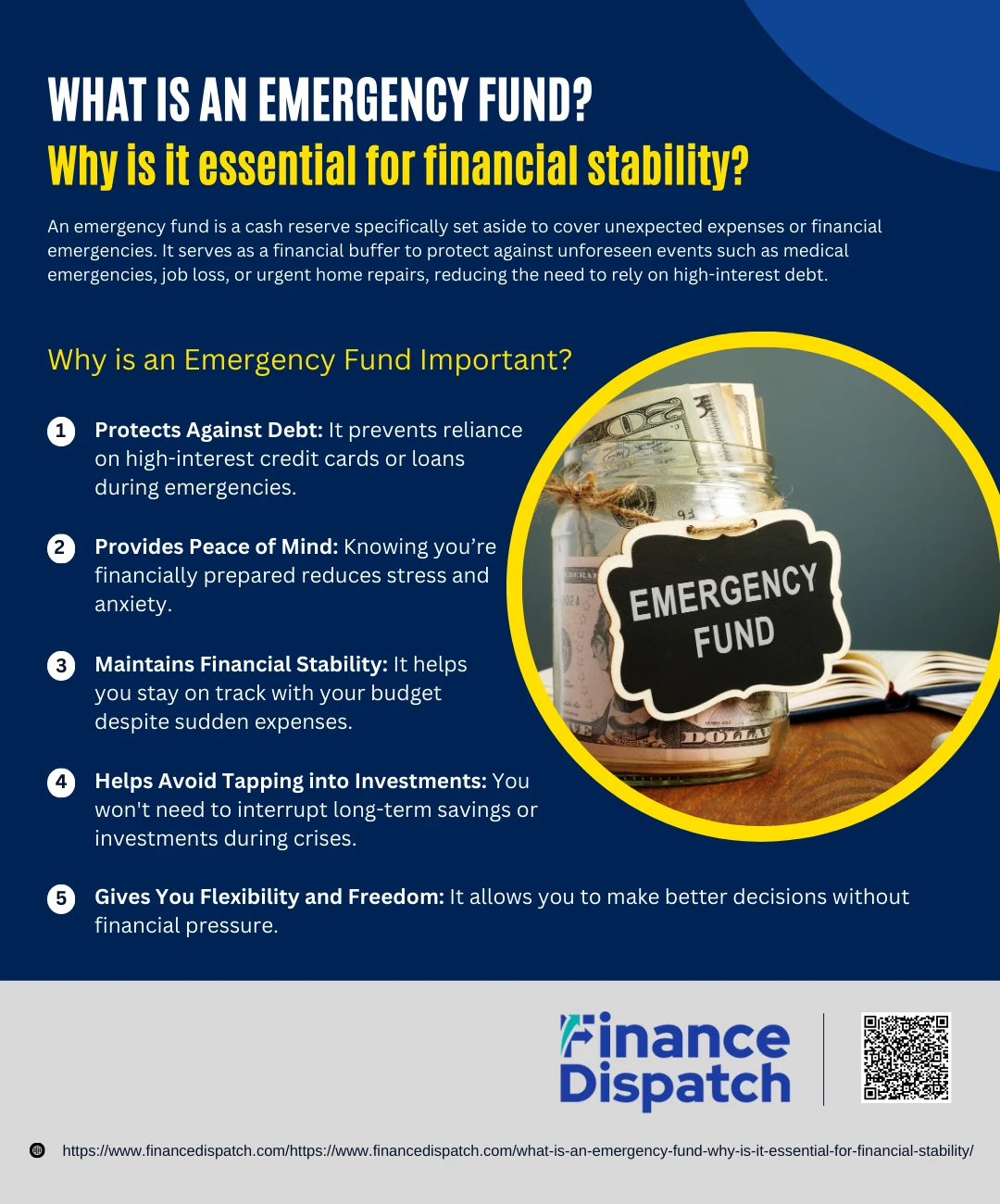

What is an Emergency Fund?

An emergency fund is a dedicated pool of money set aside specifically to cover unexpected expenses or financial emergencies. It’s not meant for planned purchases or everyday spending—instead, it serves as a financial buffer for sudden situations like medical emergencies, urgent home or car repairs, or temporary loss of income. Unlike relying on credit cards or loans, which can lead to high-interest debt, an emergency fund allows you to handle these surprises with confidence and ease. Think of it as your financial safety net—always there when you need it most, helping you stay in control and avoid financial setbacks.

Why is an Emergency Fund Important?

Why is an Emergency Fund Important?

Emergencies have a way of arriving at the worst possible times—whether it’s a sudden medical bill, an urgent car repair, or unexpected job loss. Without a financial cushion, these situations can derail your budget, force you into debt, or even lead to long-term financial instability. An emergency fund acts as a shield, protecting you from the ripple effects of life’s surprises. It ensures you’re not only able to meet immediate needs but also stay on track with your financial goals. Having this reserve brings peace of mind, reduces stress, and empowers you to handle emergencies with confidence instead of panic.

Here are several key reasons why building an emergency fund is essential:

1. Protects Against Debt

When unexpected expenses arise, many people turn to credit cards or personal loans to cover costs. These quick fixes can lead to high-interest debt that’s hard to pay off. An emergency fund allows you to avoid this cycle by using your own money instead.

2. Provides Peace of Mind

Financial uncertainty can cause immense stress. Knowing you have money set aside to handle emergencies gives you a sense of control and calm, allowing you to focus on solving the issue instead of worrying about how to pay for it.

3. Maintains Financial Stability

Without emergency savings, even small surprises can throw off your budget or force you to miss bills. A well-funded emergency account helps you maintain stability and avoid falling behind on your financial responsibilities.

4. Helps Avoid Tapping into Investments

If you don’t have cash readily available, you may feel pressured to withdraw from retirement accounts or sell investments at the wrong time. This can lead to penalties, taxes, or lost growth potential. An emergency fund protects your long-term plans from short-term setbacks.

5. Gives You Flexibility and Freedom

Life changes—sometimes suddenly. Whether it’s switching jobs, relocating, or dealing with a family emergency, having an emergency fund gives you the freedom to make decisions based on what’s best for you—not just what you can afford in the moment.

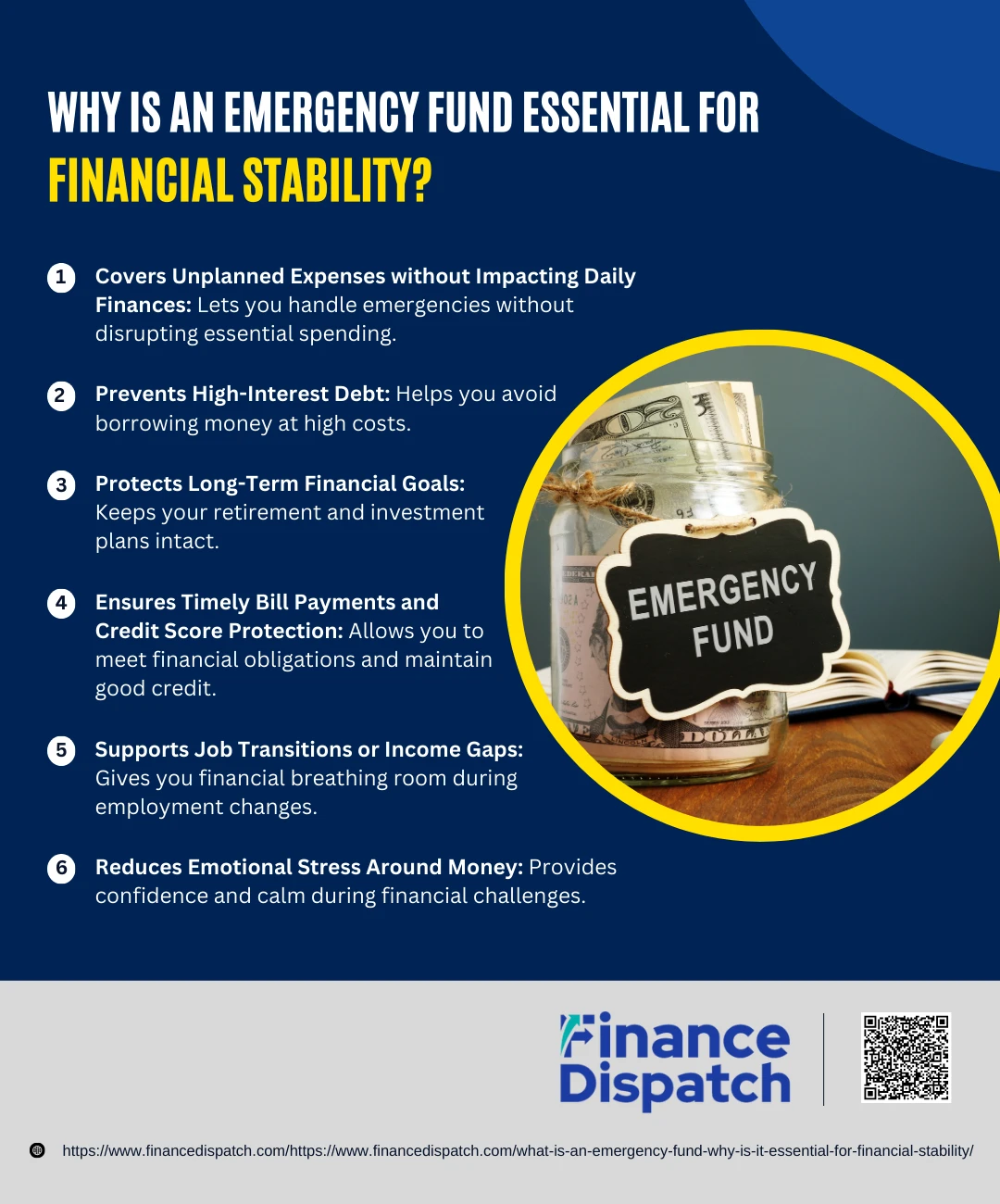

Why is it Emergency Fund Essential for Financial Stability?

Why is it Emergency Fund Essential for Financial Stability?

Financial stability isn’t just about earning a good income or having a well-planned budget—it’s also about being prepared for the unexpected. Life can throw financial curveballs at any moment, and if you don’t have a safety net, a single surprise expense can shake the foundation of your finances. That’s where an emergency fund becomes essential. It gives you the ability to respond to sudden costs without relying on credit cards, loans, or draining your long-term savings. In short, it helps you stay in control, even when life feels out of control. An emergency fund keeps your financial goals on track, protects your credit, and provides peace of mind in times of uncertainty.

Here’s how an emergency fund strengthens your financial stability:

1. Covers Unplanned Expenses without Impacting Daily Finances

Emergencies like medical bills, urgent home repairs, or car breakdowns are often impossible to predict. Having money set aside specifically for these moments means you won’t need to dip into your rent, grocery, or utility funds—keeping your daily life uninterrupted.

2. Prevents High-Interest Debt

When you don’t have emergency savings, your only fallback may be a credit card or loan. These options come with interest charges that can accumulate quickly, leading to a cycle of debt. An emergency fund helps you avoid borrowing altogether.

3. Protects Long-Term Financial Goals

Your retirement savings and investment accounts are meant for future milestones—not unexpected bills. With an emergency fund, you won’t need to compromise your long-term plans or pay penalties by withdrawing from these resources early.

4. Ensures Timely Bill Payments and Credit Score Protection

Missing even one payment can hurt your credit score, affecting your ability to borrow in the future. With an emergency fund, you can keep up with bills and financial obligations even during hard times, helping maintain your credit health.

5. Supports Job Transitions or Income Gaps

If you lose your job or experience a reduction in income, an emergency fund can sustain you for a few months while you find new work. This gives you the flexibility to look for a suitable job instead of settling out of desperation.

6. Reduces Emotional Stress Around Money

Financial stress is one of the most common causes of anxiety. Knowing you have a backup plan allows you to face emergencies calmly and confidently, rather than with panic and uncertainty.

How Much Should You Save in Your Emergency Fund?

The ideal amount to save in your emergency fund depends on your personal situation—your income, lifestyle, financial responsibilities, and job stability. While there’s no one-size-fits-all answer, a common rule of thumb is to set aside three to six months’ worth of essential living expenses. This cushion ensures that you can continue covering your basic needs—like housing, food, utilities, and transportation—during tough times, such as a job loss or medical emergency. If your income is irregular or you support a family, you may need to save even more to feel financially secure.

Below is a table to help you estimate how much you should aim to save, based on your life circumstances:

| Life Situation | Recommended Emergency Fund | Reason |

| Single, stable job | 3 months of living expenses | Lower risk and fewer dependents |

| Dual-income household | 3–4 months of living expenses | Shared income provides some buffer |

| Freelancers or self-employed | 6–12 months of living expenses | Income may be unpredictable |

| Family with children | 6+ months of living expenses | Higher responsibility and more potential for emergencies |

| High medical or housing expenses | 6+ months of living expenses | Greater risk of financial strain |

| Retired or nearing retirement | 12 months or more of living expenses | Fixed income and healthcare needs increase with age |

How to Build Your Emergency Fund

How to Build Your Emergency Fund

Building an emergency fund is one of the smartest steps you can take toward financial independence and peace of mind. It’s not about saving a huge sum all at once—it’s about developing a consistent habit of putting money aside for life’s unexpected events. Whether you’re just starting out or recovering from a recent financial setback, the process is the same: create a plan, commit to it, and stay focused. With a little patience and discipline, your emergency fund will grow over time, becoming a reliable safety net when you need it most.

Here’s a detailed step-by-step guide to help you build your emergency fund effectively:

1. Set a Realistic Goal

Start by deciding how much you want to save. A small target like $500–$1,000 is perfect for beginners and can handle minor emergencies. Eventually, aim to save at least three to six months’ worth of essential expenses (rent, groceries, bills, insurance). The more financial responsibility you have, the more you’ll want in your fund.

2. Track Your Income and Expenses

Review your monthly income and list all your expenses—both fixed and variable. Tracking your spending will reveal areas where you can cut back, giving you more room to save. Use budgeting tools or apps to simplify this process.

3. Create a Monthly Savings Target

Choose a specific amount to save each month based on your budget. Even if it’s just $25 or $50, treat it like a necessary bill you must pay—before spending on anything else. Saving consistently is more important than saving a lot at once.

4. Open a Separate Savings Account

Keep your emergency fund in a separate account from your everyday checking. This separation helps reduce the temptation to dip into it for non-emergency expenses and makes it easier to track your progress.

5. Automate Your Savings

Set up automatic transfers to move a set amount of money into your emergency fund each payday. Automating your savings takes willpower out of the equation and ensures consistent progress without the need to remember or second-guess.

6. Use Unexpected Income Wisely

Windfalls like tax refunds, work bonuses, or cash gifts are great opportunities to boost your emergency fund. Instead of spending it all, commit to putting at least half—or more—into your savings. These one-time boosts can make a big difference.

7. Start Small, Increase Gradually

If saving feels difficult right now, don’t get discouraged. Start with whatever amount is manageable. As your income grows or your expenses decrease, increase your savings contributions over time. Progress, no matter how slow, is still progress.

8. Monitor Your Progress Regularly

Check your emergency fund balance monthly or quarterly. Tracking your savings journey keeps you motivated and lets you celebrate small wins—like hitting your first $500 or $1,000.

9. Replenish After Use

If you ever need to use your emergency fund, that’s okay—that’s what it’s for. But make it a priority to rebuild it afterward. Treat replenishing it with the same urgency as building it in the first place.

Where Should You Keep Your Emergency Fund?

Choosing the right place to store your emergency fund is just as important as building it. Since emergencies can happen at any time, your savings need to be accessible, safe, and ideally earning a bit of interest while it waits. The goal is to keep your money secure but within reach—so it’s there when you really need it. That means avoiding risky investments or tying it up in long-term accounts that penalize early withdrawals. Below is a comparison of common options for storing your emergency fund, so you can decide which best suits your needs.

| Option | Accessibility | Interest Potential | Best For | Things to Consider |

| High-Yield Savings Account | Easy, 24/7 access | Moderate (1–5% APY) | Most people; balances safety and growth | Choose an FDIC-insured account with no or low fees |

| Online Savings Account | Easy, digital access | Higher than traditional | Tech-savvy users wanting better returns | May take 1–2 days to transfer funds |

| Money Market Account | Easy, some check access | Moderate to high | Larger balances, flexible access | May require a minimum balance; limited monthly withdrawals |

| Traditional Savings Account | Immediate in-person | Low | People who prefer in-branch service | Typically offers the lowest interest |

| Certificates of Deposit (CDs) | Limited (early penalties) | Higher (if long term) | Partial emergency fund or long-term tiers | Funds are locked for set periods unless laddered |

| Prepaid Debit Card | Immediate | None | Limited access to avoid overspending | Easy to access, but no interest or FDIC protection |

| Cash at Home | Immediate | None | Natural disasters, power outages | Risk of loss, theft, or damage; not recommended as primary |

When and How to Use Your Emergency Fund

An emergency fund is meant to be your financial lifeline when life throws unexpected challenges your way—but knowing when to tap into it is just as important as building it. Using it wisely ensures that the money is available when it’s truly needed and that you don’t deplete your safety net on non-essential expenses. The key is to reserve these funds for real emergencies—those unplanned, urgent situations that could disrupt your financial stability if not addressed immediately.

Here are common examples of when it’s appropriate to use your emergency fund:

- Unexpected Medical Expenses

For sudden illnesses, accidents, or procedures not covered by insurance. - Major Car Repair’s

Essential repairs that are required to keep your vehicle running safely. - Home Repairs or Appliance Replacements

Urgent issues like a leaking roof, broken furnace, or malfunctioning refrigerator. - Job Loss or Reduced Income

To cover essential living expenses like rent, groceries, and utilities until you get back on your feet. - Emergency Travel

For last-minute trips due to family emergencies such as a funeral or serious illness. - Unexpected Veterinary Costs

For urgent medical treatment of your pet that can’t be postponed. - Natural Disasters or Accidents

In cases where you need to relocate temporarily or replace damaged essentials.

Rebuilding and Maintaining Your Fund

Using your emergency fund when you truly need it is a smart financial move—but the work doesn’t end there. Once you’ve tapped into your savings, it’s essential to start rebuilding it right away. Treat it like any other financial priority, just like paying bills or rent. Even if you can only contribute a small amount each month, consistency is key. Set a new goal, adjust your budget if needed, and consider temporarily cutting back on non-essential spending to speed up the process. At the same time, maintaining your fund is an ongoing habit. Regularly check your balance, review your savings strategy, and make sure your fund still aligns with your current lifestyle and financial needs. By staying committed, you’ll ensure your safety net is always ready—no matter what life throws your way.

Conclusion

An emergency fund is more than just a savings account—it’s a vital part of your financial foundation. It offers protection, peace of mind, and the ability to handle life’s unexpected challenges without falling into debt or derailing your goals. Whether you’re facing a medical bill, job loss, or urgent home repair, having this financial cushion can make all the difference. The good news is, you don’t have to build it overnight. By starting small, saving consistently, and using it wisely, you can create a reliable safety net that brings long-term stability. Begin today—because the best time to prepare for an emergency is before it happens.