Capital gains tax (CGT) is a crucial element of financial planning that affects individuals and businesses alike. Whether you’re selling a property, parting with investments, or transferring valuable assets, understanding CGT is essential to navigate tax liabilities and optimize your returns. Unlike taxes on income or purchases, CGT specifically targets the profit, or “gain,” realized from selling an asset. However, its application varies depending on factors such as the type of asset, holding period, and your income level. This article unpacks what capital gains tax is, when it applies, and how you can manage it effectively to stay compliant and financially savvy.

What is Capital Gains Tax?

Capital gains tax (CGT) is a tax imposed on the profit earned from selling or disposing of a capital asset, such as real estate, stocks, or valuable collectibles. It applies not to the total amount received but to the “gain”—the difference between the asset’s sale price and its original purchase cost, adjusted for any improvements or allowable expenses. CGT is designed to tax wealth generated through asset appreciation and typically distinguishes between short-term gains, taxed at higher rates, and long-term gains, which often benefit from lower rates. By understanding how CGT works, individuals can better plan their financial decisions and reduce potential liabilities.

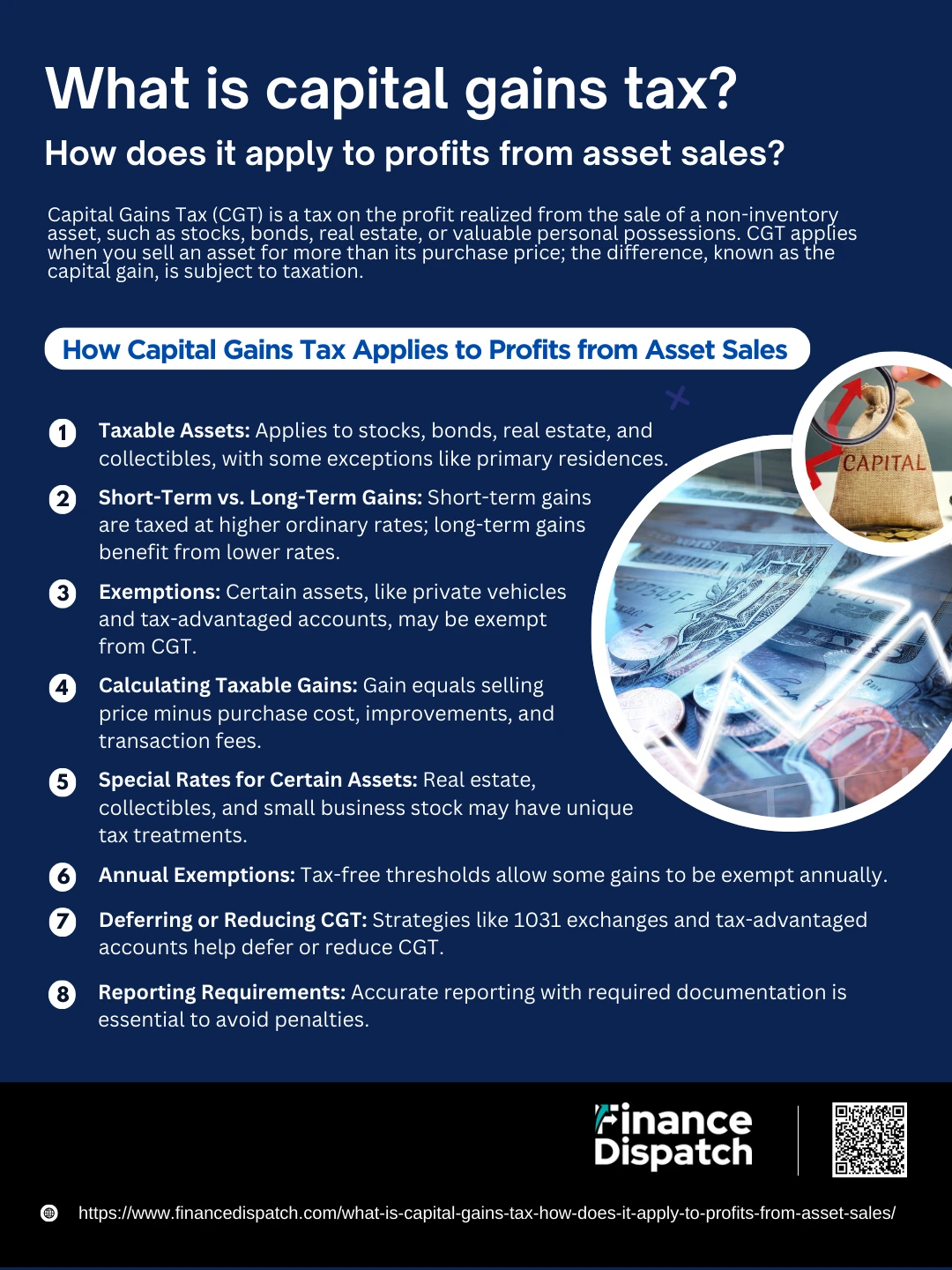

How Capital Gains Tax Applies to Profits from Asset Sales

Capital gains tax (CGT) is a levy on the profit you earn when selling or disposing of an asset that has appreciated in value. It targets the “gain”—the difference between the selling price and the purchase cost of the asset, adjusted for expenses like improvements or transaction fees. CGT is designed to tax wealth generated through asset appreciation rather than regular income. However, not all asset sales are taxed equally. Factors such as the type of asset, the holding period, and specific exemptions play a significant role in determining the tax owed. Knowing how CGT works is vital for financial planning, ensuring compliance, and optimizing after-tax returns from your investments.

Key Points About How CGT Applies to Asset Sales:

1. Taxable Assets

CGT typically applies to assets like stocks, bonds, real estate (excluding primary residences in many cases), and high-value collectibles such as art or antiques.

2. Short-Term vs. Long-Term Gains

Short-term gains (on assets held for a year or less) are taxed at higher rates, often aligning with ordinary income tax rates. Long-term gains (on assets held for more than a year) are usually taxed at lower, more favorable rates.

3. Exemptions

Some assets are exempt from CGT, such as private vehicles, gifts to charities, and gains from tax-advantaged accounts like Individual Retirement Accounts (IRAs) or 401(k)s.

4. Calculating Taxable Gains

The gain is calculated by deducting the original purchase cost, improvement expenses, and transaction costs (like brokerage fees or legal fees) from the selling price.

5. Special Rates for Certain Assets

Real estate may qualify for unique exemptions or deductions, such as exclusions for primary residences. Collectibles and small business stock may have their own specific tax rates.

6. Annual Exemptions

Many jurisdictions allow a tax-free threshold or annual exemption, meaning you can make a certain amount of gains before paying CGT.

7. Deferring or Reducing CGT

Strategies like reinvesting proceeds through 1031 exchanges for real estate or holding investments in tax-advantaged accounts can defer or reduce CGT liability.

8. Reporting Requirements

CGT must be reported accurately on your tax return, with specific deadlines and documentation, such as invoices or improvement receipts, to avoid penalties.

Types of Capital Gains

Capital gains are the profits earned from selling an asset for more than its original purchase price. These gains are categorized based on the duration for which the asset was held before being sold. Understanding the different types of capital gains—short-term and long-term—is essential for determining the tax implications and planning your financial strategy effectively.

1. Short-Term Capital Gains

Gains on assets held for one year or less before being sold. Taxed at ordinary income tax rates, which are typically higher than long-term rates. Common among day traders or investors making quick transactions.

2. Long-Term Capital Gains

Gains on assets held for more than one year before being sold. Taxed at preferential rates, which are generally lower than short-term rates. Provides a financial incentive for long-term investment strategies. Examples include profits from selling stocks, real estate, or collectibles held over a year.

3. Unrealized Capital Gains

Gains that exist when an asset has increased in value but has not yet been sold. Not subject to tax until the asset is sold and the gain is “realized.” Common in portfolios where investors hold assets to defer tax liabilities.

4. Special Cases of Capital Gains

- Real Estate Gains: Gains from selling property may qualify for unique tax treatments, such as exclusions for primary residences.

- Collectible Gains: Gains from selling collectibles like art, coins, or antiques may have distinct tax rates, often higher than long-term gains for other assets.

- Business Asset Gains: Gains from selling business assets or equipment may be taxed differently, often with options for deferrals or deductions.

Examples of Capital Gains Tax Calculations

Capital gains tax (CGT) is calculated on the profit made when selling an asset for more than its purchase cost. Understanding the calculation process is vital for accurate tax reporting and planning. Below are examples to demonstrate how CGT is determined in various scenarios, taking into account factors like holding periods, exemptions, and allowable deductions.

1. Basic Calculation for Long-Term Capital Gains

- Scenario: You purchased shares for $10,000 and sold them for $15,000 after holding them for two years.

- Calculation:

- Selling Price: $15,000

- Purchase Price: $10,000

- Capital Gain: $15,000 – $10,000 = $5,000

- Tax Rate (e.g., 15% for long-term gains): $5,000 × 15% = $750

- Result: You owe $750 in CGT.

2. Short-Term Capital Gains

- Scenario: You purchased a cryptocurrency for $8,000 and sold it for $10,000 after six months.

- Calculation:

- Selling Price: $10,000

- Purchase Price: $8,000

- Capital Gain: $10,000 – $8,000 = $2,000

- Tax Rate (based on your income, e.g., 22%): $2,000 × 22% = $440

- Result: You owe $440 in CGT.

3. Capital Gains on Real Estate with Exemption

- Scenario: You sold your primary residence for $500,000 after purchasing it for $200,000 and living in it for five years. The exemption for individuals is $250,000.

- Calculation:

- Selling Price: $500,000

- Purchase Price: $200,000

- Capital Gain: $500,000 – $200,000 = $300,000

- Exempt Amount: $250,000

- Taxable Gain: $300,000 – $250,000 = $50,000

- Tax Rate (e.g., 15% for long-term gains): $50,000 × 15% = $7,500

- Result: You owe $7,500 in CGT.

4. Capital Gains with Improvements and Costs

- Scenario: You sold a property for $400,000 that was purchased for $250,000, with $50,000 spent on improvements and $10,000 in selling expenses.

- Calculation:

- Selling Price: $400,000

- Purchase Price: $250,000

- Improvements: $50,000

- Selling Costs: $10,000

- Adjusted Basis: $250,000 + $50,000 = $300,000

- Net Gain: $400,000 – $300,000 – $10,000 = $90,000

- Tax Rate (e.g., 15% for long-term gains): $90,000 × 15% = $13,500

- Result: You owe $13,500 in CGT.

5. Capital Loss Offset

- Scenario: You sold one stock at a $10,000 profit and another at a $3,000 loss.

- Calculation:

- Total Gains: $10,000

- Total Losses: $3,000

- Net Gain: $10,000 – $3,000 = $7,000

- Tax Rate (e.g., 15% for long-term gains): $7,000 × 15% = $1,050

- Result: You owe $1,050 in CGT after offsetting the loss.

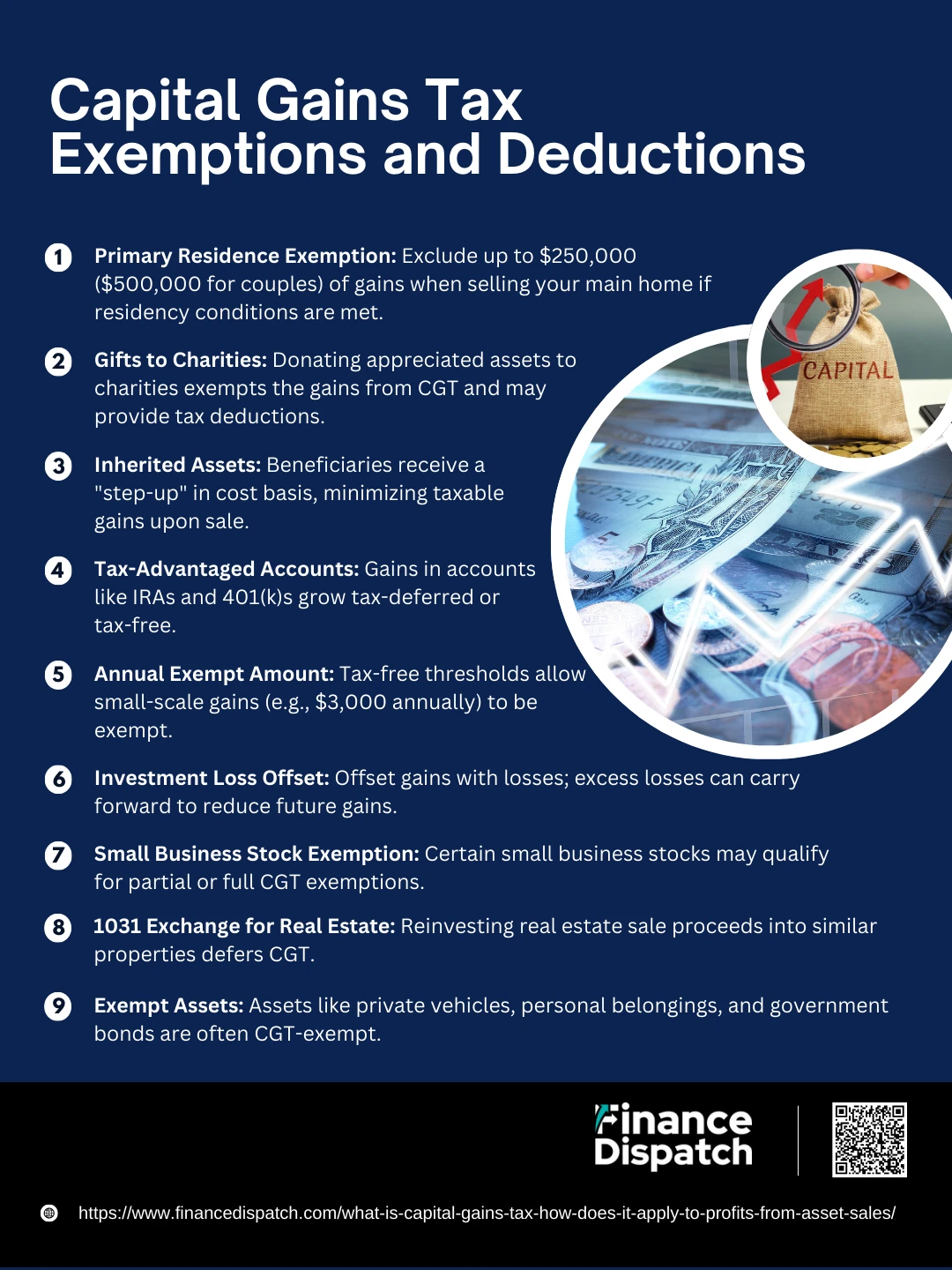

Capital Gains Tax Exemptions and Deductions

Capital gains tax (CGT) is often associated with significant tax liabilities, but there are many ways to reduce or even eliminate the tax burden. By taking advantage of exemptions and deductions, you can significantly reduce your taxable gains, whether from selling property, investments, or other assets. These provisions vary depending on the jurisdiction and type of asset, but they play a vital role in effective tax planning.

Key Exemptions and Deductions:

1. Primary Residence Exemption:

If you sell your primary home, you may qualify for a tax exemption on the first $250,000 of gains ($500,000 for married couples filing jointly). To qualify, you must have lived in the property for at least two of the last five years. This exemption does not apply to rental properties or second homes.

2. Gifts to Charities:

When you donate appreciated assets, such as stocks or real estate, to registered charities, the gains are exempt from CGT. Additionally, you may qualify for a tax deduction equal to the asset’s fair market value at the time of the donation.

3. Inherited Assets:

In many jurisdictions, beneficiaries receive a “step-up” in the cost basis for inherited assets. This means the asset’s value is adjusted to its market value at the time of inheritance, minimizing taxable gains if the asset is later sold.

4. Tax-Advantaged Accounts:

Investments held in accounts like 401(k)s, IRAs, or ISAs grow tax-deferred or tax-free. Gains are not taxed until withdrawals are made, and in some cases, such as Roth IRAs, they are never taxed.

5. Annual Exempt Amount:

Many tax systems provide a tax-free threshold for capital gains. For example, some jurisdictions allow up to $3,000 in gains to be exempt annually. This is especially useful for small-scale investors.

6. Investment Loss Offset:

Losses from investments can offset taxable gains. For instance, if you realized a $10,000 gain but incurred a $3,000 loss, your taxable gain is reduced to $7,000. Any unused losses can typically be carried forward to future years.

7. Small Business Stock Exemption:

Investments in certain small business stocks may be eligible for partial or full exemptions if held for a minimum period (e.g., five years). This incentivizes investments in startups and smaller enterprises.

8. 1031 Exchange for Real Estate:

Real estate investors can defer CGT by reinvesting the proceeds from a sale into a similar property through a 1031 exchange. This allows the tax liability to be deferred indefinitely, provided rules are followed.

9. Exempt Assets:

Certain assets are exempt from CGT, including private vehicles, personal belongings valued under a specific amount, and government-issued securities like bonds. These exemptions vary by country and asset type.

Capital Gains Tax Rates

Capital gains tax (CGT) rates vary based on several factors, including the type of asset, the duration for which it was held, and the taxpayer’s income level. Short-term gains, from assets held for one year or less, are taxed at ordinary income rates, while long-term gains benefit from lower, preferential rates. Additionally, specific assets like real estate, collectibles, or small business stocks may have unique rates. Understanding these rates is essential for accurate tax planning and compliance.

Capital Gains Tax Rates Table

| Filing Status | Short-Term Rate | Long-Term Rate (0%) | Long-Term Rate (15%) | Long-Term Rate (20%) |

| Single | Ordinary Income Rates | $0 – $48,350 | $48,351 – $533,400 | $533,401 and above |

| Married Filing Jointly | Ordinary Income Rates | $0 – $96,700 | $96,701 – $600,050 | $600,051 and above |

| Married Filing Separately | Ordinary Income Rates | $0 – $48,350 | $48,351 – $300,000 | $300,001 and above |

| Head of Household | Ordinary Income Rates | $0 – $64,750 | $64,751 – $566,700 | $566,701 and above |

Tips to Reduce Capital Gains Tax

Capital gains tax (CGT) can significantly impact your profits from asset sales, but with thoughtful planning and strategic actions, you can reduce the amount you owe. Whether you’re selling stocks, real estate, or other valuable assets, these tips can help you navigate tax rules effectively while retaining more of your earnings.

Tips to Reduce Capital Gains Tax:

1. Hold Assets for More Than One Year

By holding an asset for over a year before selling, you qualify for the lower long-term capital gains tax rate, which is significantly lower than the short-term rate that aligns with ordinary income taxes. This strategy is especially effective for investments like stocks and real estate.

2. Offset Gains with Losses

Tax-loss harvesting allows you to sell underperforming assets to offset gains from profitable ones. For instance, if you realize a $10,000 gain and a $3,000 loss, you only pay taxes on $7,000 of gains. Excess losses can also be carried forward to future tax years.

3. Utilize Primary Residence Exclusion

If you’re selling your main home, the IRS allows you to exclude up to $250,000 ($500,000 for married couples) of the capital gains, provided you’ve lived in the home for at least two of the past five years. This exclusion doesn’t apply to rental or vacation properties.

4. Invest in Tax-Advantaged Accounts

Gains from assets held in 401(k)s, IRAs, or similar accounts grow tax-deferred or tax-free. Roth accounts, for example, offer tax-free withdrawals in retirement, meaning you won’t pay CGT on your investment gains.

5. Reinvest with a 1031 Exchange

Real estate investors can defer CGT by reinvesting proceeds from a property sale into a similar property using a 1031 exchange. This defers the tax liability indefinitely, as long as the rules are followed.

6. Donate Appreciated Assets

Donating long-term appreciated assets, such as stocks or real estate, to qualified charities allows you to avoid CGT on the gains and claim a tax deduction equal to the asset’s fair market value.

7. Consider Timing of Sales

Timing asset sales when your income is lower, such as during retirement or a sabbatical year, can place you in a lower tax bracket, reducing the rate at which gains are taxed.

8. Add Improvement Costs to the Asset’s Basis

For real estate or other tangible assets, you can increase the cost basis by including the costs of significant improvements. This reduces the taxable gain when you sell the asset.

9. Leverage Small Business Stock Exemption

Certain small business stocks held for at least five years may qualify for partial or full CGT exemptions, incentivizing long-term investments in small enterprises.

10. Monitor Annual Exemptions

Many tax systems offer an annual tax-free allowance for capital gains. For example, in some jurisdictions, individuals can exclude a small portion of gains (e.g., $3,000) from taxation each year.

11. Utilize Tax-Deferred Growth Strategies

Investments in tax-deferred products, such as annuities or tax-deferred mutual funds, allow you to delay paying CGT until withdrawals are made, often in a lower tax bracket.

12. Plan Asset Transfers Strategically

If transferring assets to family members, consider gifting rather than selling, as there may be reduced or no CGT implications for gifts under certain thresholds.

Common Mistakes to Avoid

When dealing with capital gains tax (CGT), even small errors can lead to unnecessary tax liabilities or compliance issues. Missteps such as improper record-keeping, misunderstanding tax rules, or failing to plan can significantly impact your finances. By recognizing and avoiding these common mistakes, you can streamline the process, minimize taxes, and stay compliant.

Common Mistakes to Avoid:

- Failing to Hold Assets Long Enough: Selling assets too soon can subject you to higher short-term capital gains tax rates instead of the lower long-term rates, costing you more in taxes.

- Ignoring Record-Keeping: Not keeping receipts, improvement records, or purchase documents can make it difficult to calculate accurate gains and claim deductions.

- Overlooking Loss Offset Opportunities: Failing to offset gains with losses can increase your tax liability. Tax-loss harvesting is a powerful tool that many taxpayers miss out on.

- Misunderstanding Exemptions: Assuming all home sales or small-scale investments are exempt without checking eligibility for exclusions or exemptions can lead to costly errors.

- Neglecting to Plan for Tax-Advantaged Accounts: Not leveraging accounts like IRAs or 401(k)s to defer or eliminate capital gains tax can result in missed opportunities for tax savings.

- Incorrect Timing of Sales: Selling assets during a high-income year can push you into a higher tax bracket, increasing your overall tax burden.

- Breaking the Wash-Sale Rule: Selling an asset at a loss and repurchasing it within 30 days violates IRS rules, making the loss ineligible for offsetting gains.

- Failing to Report Gains: Not reporting capital gains on your tax return, even when the proceeds are reinvested, can lead to penalties and audits.

- Underestimating Estate Planning: Ignoring the step-up in basis for inherited assets or failing to account for gifting strategies can result in higher taxes for you or your heirs.

- Missing Filing Deadlines: Forgetting to report and pay CGT by the required deadlines can incur penalties and interest, increasing your overall liability.

Conclusion

Understanding capital gains tax (CGT) is essential for managing your financial decisions effectively and minimizing tax liabilities. Whether you’re selling investments, real estate, or other assets, knowing the applicable rules, exemptions, and strategies can help you retain more of your profits. Avoiding common mistakes, such as poor record-keeping or failing to leverage exemptions, ensures compliance while optimizing your financial outcomes. By planning strategically and consulting with tax professionals, you can navigate CGT with confidence, safeguard your wealth, and make informed decisions that align with your financial goals.