When it comes to managing your wealth effectively, understanding your risk tolerance is essential. Risk tolerance refers to your ability and willingness to endure fluctuations in the value of your investments. It’s not just about how much risk you’re willing to take but also about how well your financial goals, emotional resilience, and time horizon align with that risk. By identifying your comfort level with uncertainty, you can create a personalized investment strategy that balances growth opportunities with the stability you need. Understanding risk tolerance isn’t just a technical financial exercise; it’s the foundation for achieving your long-term financial goals while maintaining peace of mind along the way.

What is Risk Tolerance?

Risk tolerance is the degree of uncertainty you’re comfortable with when it comes to your investments. It reflects how much potential loss you’re willing to accept in pursuit of higher returns. This concept is deeply personal and varies from one individual to another based on factors like financial goals, emotional resilience, and time horizon. For example, someone with a high risk tolerance might prefer aggressive investments like stocks or high-yield bonds, while a person with low risk tolerance may opt for safer options like government securities or fixed deposits. Understanding your risk tolerance is not just about knowing your preferences; it’s about aligning your investment strategy with your financial capacity and comfort level, ensuring a more sustainable path toward wealth accumulation.

Why Understanding Risk Tolerance is Essential for Wealth Management

Why Understanding Risk Tolerance is Essential for Wealth Management

Risk tolerance is the cornerstone of effective wealth management. It determines how well your financial strategies align with your ability to handle investment risks, ensuring that your portfolio remains both sustainable and manageable over time. Without a clear understanding of your risk tolerance, you may find yourself either overstressed by market volatility or missing out on potential growth opportunities.

Key Reasons Why Risk Tolerance is Crucial:

1. Customized Investment Strategies

Your risk tolerance acts as a guide for designing an investment portfolio that suits your unique financial profile. For instance, if you are a risk-averse individual, your portfolio might emphasize stable, low-risk assets such as bonds or money market funds. On the other hand, if you have a high tolerance for risk, your investments could lean more heavily toward stocks or other high-growth opportunities. This customization ensures your financial plan reflects your comfort level while still targeting your desired goals.

2. Minimized Emotional Stress

Market volatility can be stressful, especially if your investments expose you to more risk than you’re comfortable with. Understanding your risk tolerance helps you prepare emotionally for the ups and downs of the market, reducing panic-driven decisions. For example, when markets dip, someone with a clear understanding of their risk tolerance is more likely to stay the course instead of selling at a loss.

3. Better Alignment with Financial Goals

Different financial goals require different levels of risk. A clear understanding of your risk tolerance allows you to match your investment strategies with your goals. For example, saving for retirement in 30 years may justify a higher-risk portfolio, while saving for a down payment in three years would require a more conservative approach. This alignment ensures your financial goals are both achievable and secure.

4. Enhanced Financial Discipline

Risk tolerance provides a framework for disciplined investing, preventing you from chasing high-risk opportunities during bullish markets or overcorrecting during bearish ones. By maintaining a strategy that respects your risk limits, you develop better financial habits, such as patience and long-term planning.

5. Improved Risk-Reward Balance

Every investment involves a trade-off between risk and reward. Understanding your risk tolerance enables you to balance high-risk, high-reward investments with safer options. This balance optimizes your portfolio’s potential for growth while safeguarding your financial stability.

6. Adaptability to Life Changes

As your life evolves—whether due to career changes, family needs, or approaching retirement—your risk tolerance may shift. Recognizing and revisiting your tolerance helps you adjust your investment strategy to reflect these new circumstances, ensuring your portfolio continues to meet your changing needs.

7. Reduced Financial Losses

Taking on more risk than you can handle often leads to poor decisions and unnecessary financial losses. When you understand your tolerance for risk, you are less likely to engage in speculative investments that don’t align with your capacity for potential downturns, protecting your wealth over the long term.

Factors Influencing Risk Tolerance

Risk tolerance is not static; it is influenced by a wide range of personal and external factors that shape how much risk you are willing and able to take in your investment journey. These factors work together to determine your financial comfort zone, ensuring that your investment strategy aligns with your goals and life circumstances. A deeper understanding of these influences helps you make confident, informed decisions while navigating the uncertainties of wealth management.

Key Factors Influencing Risk Tolerance:

Key Factors Influencing Risk Tolerance:

1. Age

Age is one of the most significant factors in determining risk tolerance. Younger investors often have the luxury of time to recover from potential losses, allowing them to take on riskier investments with higher growth potential. In contrast, those nearing retirement typically prioritize capital preservation, opting for more stable, low-risk investments.

2. Income Level

A higher and more stable income provides a financial cushion, enabling greater risk tolerance. Individuals with consistent earnings can afford to invest in volatile markets, knowing they have other income sources to rely on. On the other hand, those with lower or uncertain incomes may favor safer, less volatile investment options to avoid jeopardizing their financial stability.

3. Financial Goals

The purpose of your investment greatly influences your approach to risk. For instance, if you are saving for a long-term goal like retirement, you may be more open to taking risks for higher returns. However, short-term goals, such as saving for a house or a child’s education, often require a conservative approach to protect against short-term market volatility.

4. Investment Experience

Experience and knowledge in investing significantly affect your comfort with risk. Seasoned investors, familiar with market dynamics and fluctuations, are generally more confident in taking calculated risks. Newer investors may be more cautious, as they lack the experience to handle volatile situations calmly.

5. Time Horizon

The length of time you have to achieve your financial objectives plays a critical role in determining risk tolerance. Longer time horizons allow for riskier investments because there is sufficient time to recover from market downturns. Conversely, a shorter time horizon necessitates safer investments to ensure stability.

6. Personal Temperament

Your natural disposition toward risk greatly impacts your investment decisions. If you are inherently cautious, you may prefer steady, low-risk options even if they offer modest returns. Conversely, an adventurous individual might seek out high-growth opportunities despite the potential for higher volatility.

7. Market Conditions

Economic trends, geopolitical developments, and overall market volatility can influence your risk tolerance. For example, during periods of economic stability, you might feel more confident in taking risks, while in uncertain times, your tolerance for risk may decrease.

8. Family and Financial Responsibilities

Individuals with dependents or significant financial obligations, such as mortgages or education expenses, often lean toward conservative investments. Their focus is on ensuring financial security for their family, which may limit their willingness to take on high-risk ventures.

Types of Risk Tolerance

Risk tolerance varies among individuals, influencing the way they approach investment decisions and handle financial uncertainties. It generally falls into distinct categories, each characterized by unique behaviors, preferences, and levels of comfort with market volatility. Understanding these types is essential for tailoring your investment strategy to your personal risk profile.

Key Types of Risk Tolerance:

1. Aggressive Risk Tolerance

Individuals with aggressive risk tolerance are willing to accept significant market volatility and potential losses in pursuit of higher returns. They typically invest heavily in stocks, emerging markets, or other high-risk, high-reward options. This type is most common among younger investors with long-term financial goals and a high capacity for recovery.

2. Moderate Risk Tolerance

Moderate investors strike a balance between risk and reward. They are comfortable with a mix of growth-focused investments, like stocks, and stability-oriented assets, such as bonds. This approach appeals to those who want growth but are cautious about excessive market exposure.

3. Conservative Risk Tolerance

Those with conservative risk tolerance prioritize capital preservation over potential gains. They often invest in low-risk, stable options, such as government bonds, fixed deposits, or money market funds. This type is prevalent among retirees or individuals with short-term financial goals and limited capacity for losses.

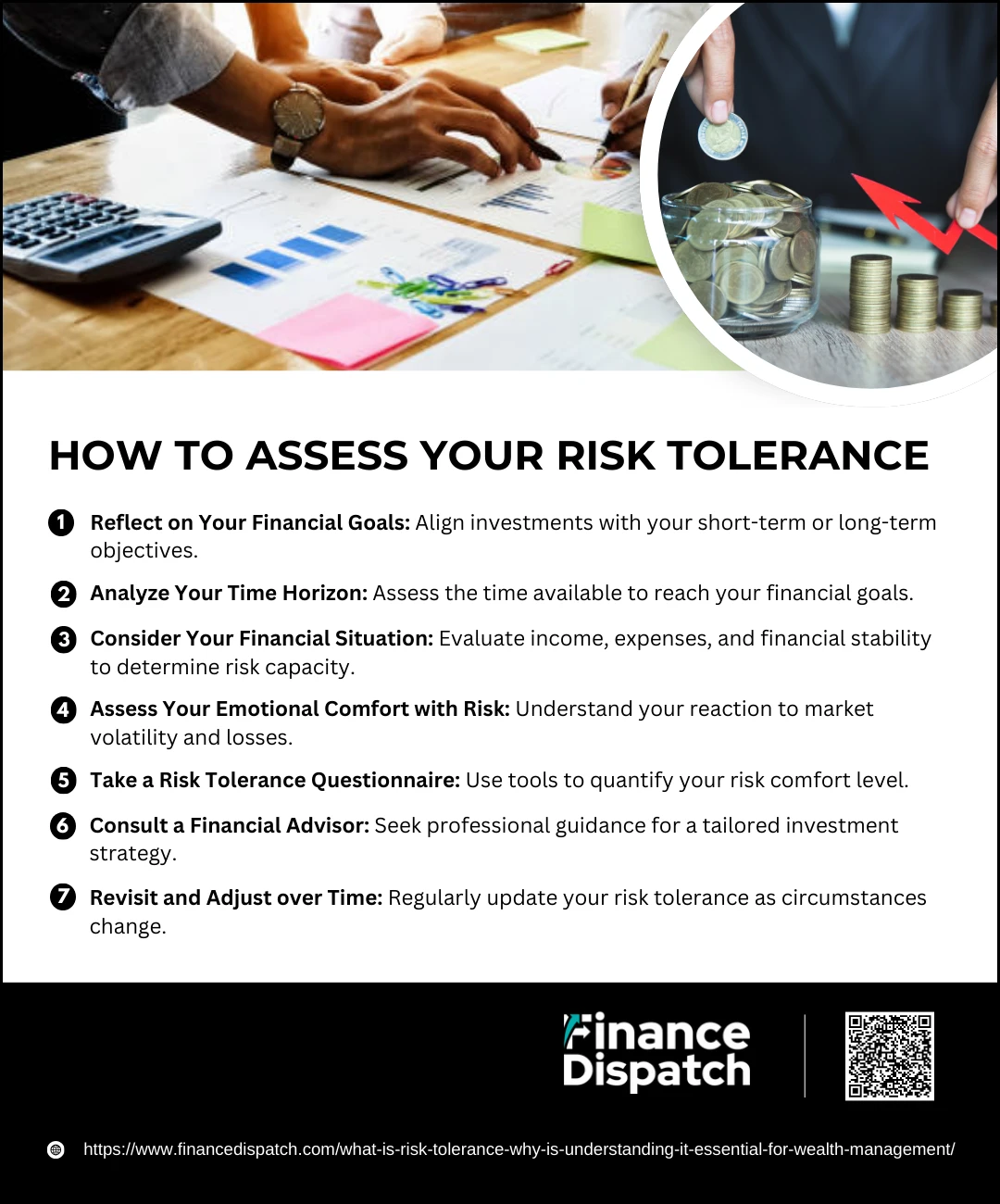

How to Assess Your Risk Tolerance

How to Assess Your Risk Tolerance

Understanding your risk tolerance is essential for building an investment strategy that suits your goals and emotional comfort. Your risk tolerance reflects not only your willingness to take risks but also your financial capacity to absorb potential losses. A thorough assessment allows you to align your portfolio with your objectives, minimize stress, and stay focused during market fluctuations. Here’s how you can evaluate your risk tolerance in a structured way:

Steps to Assess Your Risk Tolerance:

1. Reflect on Your Financial Goals

Begin by clarifying why you are investing. Long-term goals like retirement or wealth accumulation may allow for higher levels of risk, as you have time to recover from potential losses. Conversely, short-term goals, such as saving for a down payment or a child’s education, may require a more conservative approach to protect your funds from market volatility.

2. Analyze Your Time Horizon

Your time horizon is the amount of time you have before needing to access your investments. If you have decades to invest, you can afford to take on more risk, as market fluctuations tend to smooth out over time. For shorter time frames, however, stability becomes crucial to ensure funds are available when needed.

3. Consider Your Financial Situation

Take a close look at your current income, expenses, savings, and liabilities. A strong financial position—characterized by steady income and a robust emergency fund—may enable you to handle higher-risk investments. On the other hand, if your finances are tight or unpredictable, a conservative approach may be more appropriate to safeguard your principal.

4. Assess Your Emotional Comfort with Risk

Think about how you typically respond to financial losses or market downturns. If you find market volatility stressful and struggle to sleep during turbulent periods, a lower-risk portfolio might be better suited to your temperament. Conversely, if you can stay calm and focused during market dips, you may have a higher tolerance for risk.

5. Take a Risk Tolerance Questionnaire

Many financial institutions and online platforms provide risk tolerance assessments. These questionnaires ask targeted questions about your investment preferences, time horizon, and emotional response to losses, helping you quantify your comfort with various risk levels.

6. Consult a Financial Advisor

A professional advisor can help you navigate the complexities of assessing risk tolerance. They combine insights from your financial situation, goals, and personal preferences to design a portfolio that balances risk and reward effectively. They can also provide guidance on adjusting your investments over time as circumstances change.

7. Revisit and Adjust Over Time

Risk tolerance is not static; it evolves with life events, financial milestones, and changes in market conditions. For instance, your willingness to take risks may decrease as you near retirement or if you experience significant changes in income or responsibilities. Regularly reviewing and adjusting your risk tolerance ensures that your investment strategy remains aligned with your current situation and future goals.

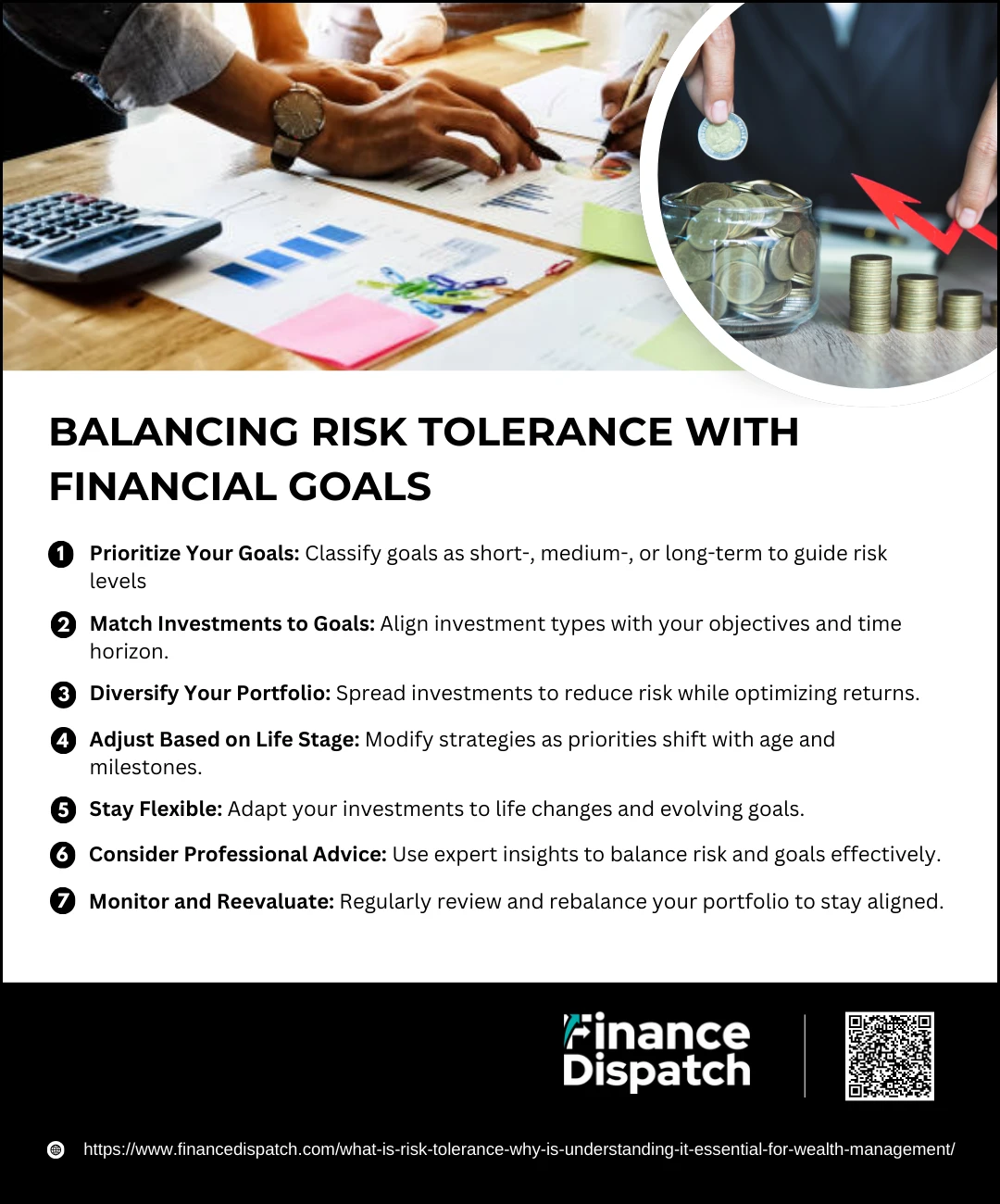

Balancing Risk Tolerance with Financial Goals

Balancing Risk Tolerance with Financial Goals

Balancing your risk tolerance with your financial goals is a vital aspect of successful wealth management. Risk tolerance dictates how much uncertainty you’re comfortable with, while your financial goals define what you’re aiming to achieve. By aligning these two elements, you can create a strategy that ensures both financial growth and emotional comfort, enabling you to stay committed to your long-term plans.

Tips for Balancing Risk Tolerance with Financial Goals:

- Prioritize Your Goals

Categorize your financial goals as short-term, medium-term, or long-term. Short-term goals, like saving for a vacation, may require low-risk investments, whereas long-term goals, such as retirement, can accommodate higher risk for greater returns. - Match Investments to Goals

Choose investment vehicles that align with both your risk tolerance and the time horizon of your goals. For example, stocks may suit long-term growth goals, while bonds or fixed deposits are better for short-term stability. - Diversify Your Portfolio

Spread your investments across various asset classes to balance risk and reward. Diversification reduces the impact of any single investment’s poor performance and aligns your portfolio with your risk tolerance. - Adjust Based on Life Stage

As your financial priorities evolve, so should your investment strategy. Younger individuals may take on more risk to maximize growth, while older investors nearing retirement may shift toward preserving capital. - Stay Flexible

Life changes, such as career transitions or family additions, can alter your financial situation and goals. Regularly reassess your risk tolerance and adjust your portfolio to reflect new circumstances. - Consider Professional Advice

A financial advisor can help you navigate the complexities of aligning risk tolerance with goals. They can recommend strategies that fit your profile and adjust them as needed. - Monitor and Reevaluate

Periodically review your investments to ensure they are performing in line with your expectations and goals. Rebalancing your portfolio helps maintain alignment with your risk tolerance and financial objectives.

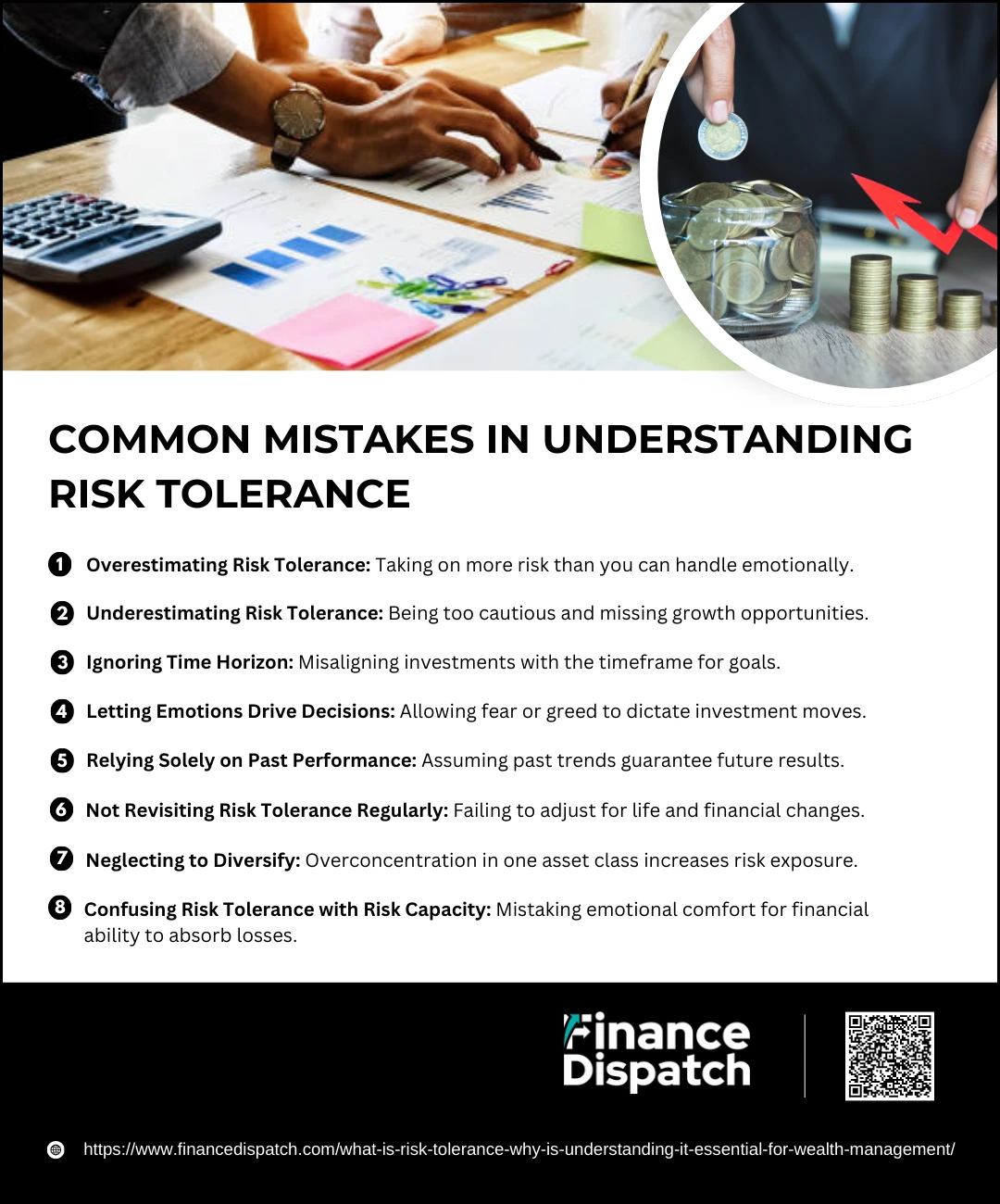

Common Mistakes in Understanding Risk Tolerance

Common Mistakes in Understanding Risk Tolerance

Understanding risk tolerance is a critical part of building a sound financial strategy, but it’s an area where many people go wrong. Misjudging your risk tolerance can lead to poor investment decisions, unnecessary stress, or missed opportunities for growth. By recognizing these common mistakes, you can avoid pitfalls and create a more balanced and effective financial plan.

Common Mistakes in Understanding Risk Tolerance:

1. Overestimating Risk Tolerance

Many people believe they can handle more risk than they actually can, leading to panic and impulsive decisions during market downturns.

2. Underestimating Risk Tolerance

Conversely, being overly cautious may result in missed opportunities for growth, particularly for long-term goals.

3. Ignoring Time Horizon

Failing to consider how long you have to reach your financial goals can lead to mismatched investment strategies. Short-term goals require lower risk, while long-term objectives can accommodate higher risk.

4. Letting Emotions Drive Decisions

Emotional reactions, such as fear during market dips or greed during bull markets, can distort your perception of risk and derail your strategy.

5. Relying Solely on Past Performance

Assuming that past market trends will continue can lead to a false sense of security or an overestimation of potential returns.

6. Not Revisiting Risk Tolerance Regularly

Risk tolerance is not static. Life changes, such as marriage, career shifts, or nearing retirement, should prompt a reassessment of your comfort with risk.

7. Neglecting to Diversify

Concentrating investments in a single asset class or sector can increase your risk exposure, even if your tolerance suggests otherwise.

8. Confusing Risk Tolerance with Risk Capacity

Risk tolerance reflects your emotional comfort with risk, while risk capacity is your financial ability to absorb losses. Mixing the two can result in inappropriate investment decisions.

How Financial Advisors Use Risk Tolerance in Wealth Management

Financial advisors play a crucial role in aligning your risk tolerance with a personalized wealth management strategy. They begin by assessing your risk tolerance through tools like questionnaires, discussions, and analysis of your financial goals and situation. This understanding helps them design an investment portfolio that balances potential returns with your comfort level and financial capacity. Advisors also use your risk tolerance to determine asset allocation, deciding how much of your portfolio should be invested in stocks, bonds, or other asset classes. Additionally, they periodically revisit your risk tolerance to ensure your strategy evolves with life changes, market conditions, and shifting financial priorities. By incorporating risk tolerance into their approach, financial advisors help you achieve your goals while minimizing stress and maintaining a sustainable investment plan.

Conclusion

Understanding risk tolerance is fundamental to building a successful financial strategy and achieving long-term goals. It serves as a guide for making informed investment decisions that align with your emotional comfort, financial capacity, and time horizon. Whether you’re working independently or with a financial advisor, accurately assessing and applying your risk tolerance ensures that your portfolio reflects your unique needs and priorities. By avoiding common mistakes and regularly revisiting your risk profile, you can navigate market uncertainties with confidence and stay on track toward financial stability and growth. Balancing risk with opportunity is the key to sustainable wealth management and a secure financial future.